Official Site of The State of New Jersey

Official Site of The State of New Jersey

A Performance Audit of Employee Benefits: City of Brigantine

Table of Contents

- Posted on - 12/1/2022

- Audit Authority, Background, and Executive Summary

- Audit Objectives, Scope, and Methodology

- Audit Findings and Recommendations

- Reporting Requirements

Audit Authority, Background, and Executive Summary

We performed this audit pursuant to the State Comptroller’s authority set forth in N.J.S.A. 52:15C-1 et seq. We conducted this performance audit in accordance with Generally Accepted Government Auditing Standards (GAGAS)[1] applicable to performance audits. Those standards require that we plan and perform the audit to obtain sufficient, appropriate evidence to provide a reasonable basis for our findings and conclusions based on our audit objectives. We believe that the evidence obtained provides a reasonable basis for our findings and conclusions based on our audit objectives.

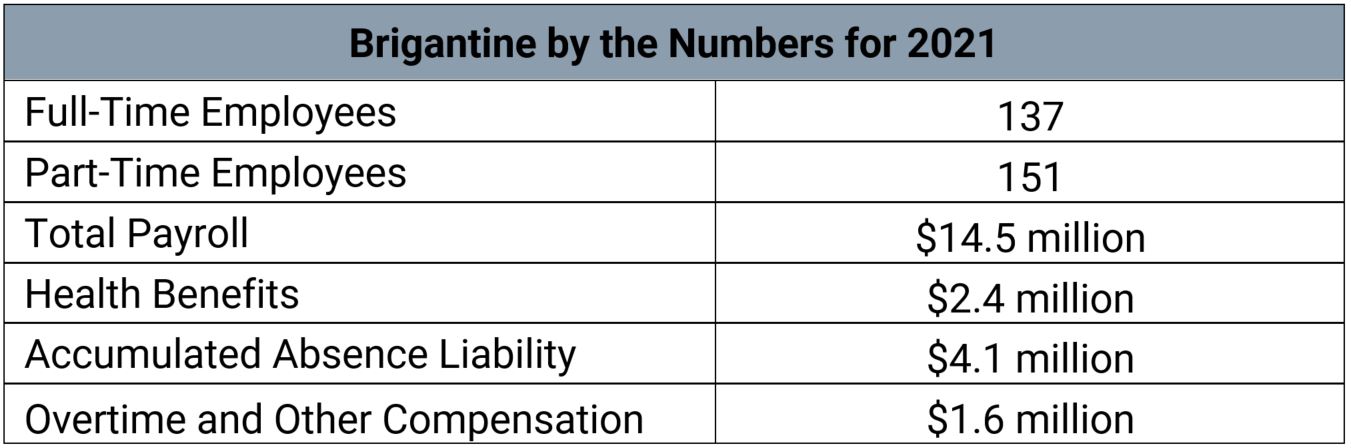

The City of Brigantine (City or Brigantine) is a municipality in Atlantic County, New Jersey. United States Census data as of April 2020 estimates that the City’s population was 7,716. Brigantine covers an area of 6.52 square miles. The City operates under a Council-Manager form of government.

Most of Brigantine’s full-time employees are covered by a collective bargaining agreement (CBA). According to the City’s 2021 Employee Handbook, Brigantine recognizes eight bargaining units. Each bargaining unit separately negotiates with the City to define terms of employment, including pay, work hours, and benefits for union members. Terms of employment for employees not covered by a CBA are established by either an individual employment contract or the Employee Handbook.

Our audit identified weaknesses with certain fiscal and operating practices related to employee benefits. Our audit found that the City lacked adequate policies, procedures, and controls governing the functions of personnel, payroll, and procurement.

Specifically, our audit found that Brigantine failed to:

- Adhere to state laws and its own agreements regarding the payment and use of accrued sick and vacation leave;

- Follow its policies regarding overtime, compensatory time, and nepotism;

- Administer health benefit waiver payments appropriately, resulting in wasteful payments of approximately $64,500;

- Substantiate data received from its health insurance broker, resulting in the potential loss of $191,000 in healthcare savings; and

- Properly administer and fund its lifeguard pension plan, leading to a $4.5 million unfunded plan liability.

The City must take appropriate action to strengthen its internal controls to improve its current practices in order to achieve greater operational effectiveness and improve compliance with applicable laws and regulations.

We make 15 recommendations to improve Brigantine’s operations and its compliance with applicable statutes and regulations.

Audit Objectives, Scope, and Methodology

The objectives of our performance audit were to review the City’s controls over employee benefits, assess its compliance with laws, regulations, and internal policies and procedures concerning those benefits, and identify cost savings involving health insurance.

The period January 1, 2019 through December 31, 2021

To accomplish our objectives, we reviewed relevant statutes, regulations, Brigantine’s policies and procedures, CBAs, financial and payroll records, and other supporting documentation. We also interviewed certain personnel to understand their job responsibilities, overall operations, and Brigantine’s internal controls.

GAGAS requires auditors to plan and perform audit procedures to assess internal control when internal control is determined to be significant to the objective. The Government Accountability Office’s Standards for Internal Control in the Federal Government, or “Green Book,”[2] provides a framework for internal control systems for public entities. The Green Book establishes five components of an internal control system: control environment, risk assessment, control activities, information and communication, and monitoring. The five components include 17 principles that support the effective design, implementation, and operation of an internal control system.

As part of our review, we selected a judgmental sample of records. Our samples were designed to provide conclusions about the validity of the sampled transactions and the adequacy of internal controls and compliance with applicable laws, regulations, policies, and procedures. Because we used a non-statistical sampling approach, the results of our testing cannot be projected over the entire population of like transactions or contracts.

Audit Findings and Recommendations

A. Sick and Vacation Leave Limits

Objective: To determine whether whether the City’s CBAs, individual employment contracts, and Employee Handbook complied with statutory limits on sick and vacation leave.

Finding

The City’s CBAs, employment contracts, and Employee Handbook did not comply with applicable state laws pertaining to the payment and accrual of unused sick and vacation leave for employees hired after May 21, 2010.

Criteria

The Legislature enacted P.L. 2010, Chapter 3[3] in March 2010 to amend and supplement statutes concerning benefits for public employees. The 2010 law applied earlier sick and vacation leave reforms to all employees hired after May 21, 2010. The 2010 law prohibited payments for unused sick leave over $15,000 and required that payment to be made only upon retirement from a local or state pension system. The 2010 law also limited vacation carryover to one year’s worth, which means that vacation leave may be lost if not used the year after it was initially awarded. The City has established additional sick and vacation leave policies through CBAs, individual employment contracts, and the Employee Handbook.

Methodology

To meet this objective, we:

- Interviewed the city manager and personnel director to understand the procedures regarding the authorization, approval, and documentation of unused sick time payments; and

- Reviewed the Employee Handbook, CBAs, and individual employment contracts related to sick and vacation leave.

Audit Results

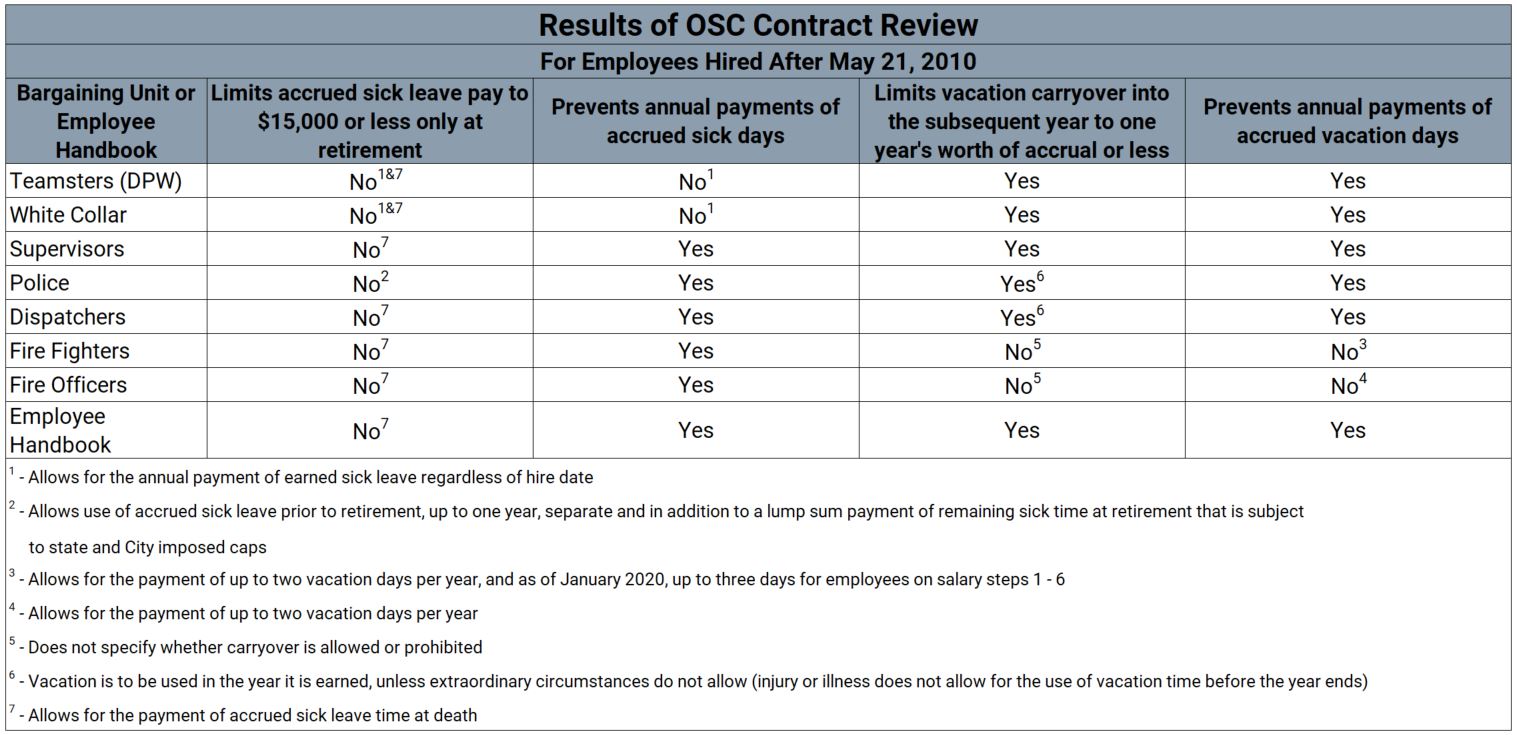

Our review of the sick and vacation leave provisions found terms in seven of the eight applicable CBAs and the 2021 Employee Handbook that failed to comply with statutory requirements. The chart below shows the results of our review.

All of the reviewed CBAs as well as the Employee Handbook allowed payments for unused sick leave at a time other than retirement for employees hired after May 21, 2010. This violates N.J.S.A. 40A:9-10.4, which caps unused sick time payments at $15,000 and prohibits such payments from being made other than at retirement from a local or state pension program. Specifically, we identified two CBAs – Teamsters (DPW) and White Collar employees – that allowed for the annual payment of unused sick leave without limiting those payments to those hired prior to May 21, 2010. Additionally, we identified a change in the current police CBA, effective January 2021, that allows employees hired after May 21, 2010 to use a calendar year’s worth of accrued sick leave prior to retirement in addition to receiving a payment for sick leave at retirement capped at $15,000. This leave violates both the requirement for payment of accrued sick leave at retirement only and the state-imposed cap of $15,000 for employees hired after May 21, 2010. Similar treatment of the use and payment for accumulated leave time prior to retirement was identified in OSC’s report titled “A Review of Sick and Vacation Leave Policies in New Jersey Municipalities”[4]as unlawful compensation.

Our review also identified two CBAs that did not include specific language to limit vacation carryover into the subsequent year to one year’s worth of accrued time. These same agreements allowed for the annual payment of accrued vacation days. As noted in our report mentioned above, “the practice of converting unused vacation time or allowing payment for unused time may contravene the intent of the Legislature in enacting the vacation leave reforms.”[5]

Finally, our review of six individual employment contracts found that the chief financial officer’s (CFO) contract allows for the payment of up to one calendar year, or 2,080 hours, of accumulated sick leave at retirement and allows carryover of 50 vacation days per year. The City hired the CFO in 2015, and the CFO is therefore subject to the 2010 state law that limits payments for sick leave and carryover of vacation leave. Although City documents show that the CFO is capped at $15,000, the CFO’s contract expressly allows for the payment of 2,080 hours of accumulated sick leave to the extent permissible by law. By simply referring to state law and not identifying what state law requires, the contract presumes that employees responsible for administering the payments will either know or research state law on this topic, which unnecessarily increases the risk that the law will not be followed. City records also show that the CFO earned 30 vacation days in 2021 and carried 50 unused vacation days into 2022. The carryover of 50 days is 20 days more than allowed by the 2010 law.

Cause

Brigantine did not incorporate the sick and vacation leave limits established in the 2010 law into the City’s CBAs, individual employment contracts, or Employee Handbook.

Effect/Potential Effect

Failure to integrate the sick and vacation leave limits provided by the 2010 law undermines the cost-savings intent afforded by the law and exposes taxpayers to costly leave benefit payments.

Recommendations

- Seek advice from counsel regarding amendments to CBAs, individual employment contracts, and the Employee Handbook to include the requirements of the 2010 law. Limit sick leave payments to employees hired after May 21, 2010 to $15,000 and only upon retirement. Ensure vacation leave may not accrue for more than one year after the vacation leave was initially awarded.

- Perform an assessment of employee leave balances to determine if adjustments are warranted in order to comply with the 2010 law and make appropriate adjustments.

B. Accumulated Leave Payments

Objective: To determine whether accumulated leave payments were in accordance with statutes, regulations, and CBAs.

Finding

Brigantine did not obtain the required documentation for retiring employees using sick leave, resulting in the undocumented and potentially wasteful use of 165 sick days valued at $57,000.

Brigantine did not accurately calculate the earned leave time of retirees in accordance with employment contracts and CBAs, resulting in $10,900 of improper payments.

Criteria

- The City’s CBAs, individual employment contracts, and Employee Handbook outline the number of accumulated leave days employees are entitled to; establish guidelines for the use and payment of said benefits; and impose limits for sick leave use on consecutive days and use exceeding a specific amount annually. Employees are required to obtain and submit medical documentation to the City to substantiate the use of sick leave in excess of established limits.

- The City’s CBAs, individual employment contracts, and Employee Handbook also establish guidelines for the proration of accrued leave benefits based on terminal leave or retirement date Terminal leave allows an employee to use accumulated leave to remain on the payroll for an extended time prior to retirement and without actually working.

Methodology

To meet this objective, we:

- Interviewed the city manager and personnel director to understand the procedures regarding the authorization, approval, and documentation of sick time usage;

- Examined the Employee Handbook, CBAs, and individual employment contracts related to sick time and the proration of accrued leave time; and

- Examined sick leave usage for all employees retiring between 2019 through 2021.

Audit Results

Our review of sick leave usage prior to retirement for 15 employees found that the City did not consistently obtain medical documentation when necessary. We identified nine employees that used 469 sick days leading up to their retirement. Testing found that 165, or 35 percent, of the used sick days were unsupported and valued at $57,000. For example, one employee used 97 of 127 sick days without submitting a doctor’s note. These 97 unsupported sick days were valued at $25,000. We note that none of these employees were subject to the caps established by the 2010 law.

Furthermore, our review determined that the City did not accurately prorate accumulated leave benefits based on the retirement date or when the employee commenced the use of terminal leave as required in its CBAs. The CBAs include provisions requiring the proration, or adjustment, of an employee’s unused leave time balances using the employee’s terminal leave or retirement date. The CBAs require that the City allow employees to only earn leave time up to their retirement date or when terminal leave commences. For example, the police CBA states that “[e]mployees shall not continue to accrue any additional benefits, including salary increases and supplemental incentives (vacation, sick, etc.) while on terminal leave.” Our testing indicated that the City did not always prorate earned leave time according to the applicable CBA, resulting in improper payments of $10,900. One employee improperly earned and used approximately $10,100 of leave time that was not prorated while on terminal leave.

Cause

Brigantine did not adhere to contractual requirements to obtain medical documentation to substantiate employee absences and did not prorate accumulated leave benefits based on terminal leave and retirement dates as prescribed in its CBAs.

Effect/Potential Effect

Failure to enforce sick leave policies allowed for the potentially wasteful use of 165 accumulated sick days valued at $57,000. Inaccurate calculations of prorated leave benefits resulted in improper payments of unearned sick leave to retiring employees valued at $10,900. Failure to enforce policies led to these wasteful payments and may continue to do so in the future.

Recommendations

3. Enforce current policies regarding the proration of accumulated leave time for separating employees and doctor’s note requirements to prevent abuse or misuse of accumulated sick leave.

4. Develop and implement a process for the calculation and review of payments to employees who have terminated their employment to ensure payments include only eligible earned leave time.

C. Overtime Compliance

Objective: To determine whether Brigantine’s system of internal controls for the payment of overtime wages was sufficient.

Finding

The City did not follow its policies related to overtime, compensatory time, and nepotism.

Criteria

Federal overtime requirements are contained in the Fair Labor Standards Act (FLSA).[6] Unless exempt, employees covered by FLSA must receive overtime pay when more than 40 hours are worked in a workweek at the rate of one and one-half their regular rate of pay.[7] FLSA requires evidence of daily and weekly hours worked to substantiate an employer’s compliance with FLSA. Compensatory time is paid time off that is earned and accrued by employees in lieu of time-and-a-half overtime wages for working overtime hours. Employees can use the accrued time off at a later date. The use of compensatory time instead of overtime is limited by 29 U.S.C. § 207 of the U.S. Code to a public agency that is a state, a political subdivision of a state, or an interstate governmental agency. Employees engaged in law enforcement, fire protection, emergency response activities, and employees engaged in seasonal activities may accrue up to 480 hours of compensatory time each year. All other state and local government employees may accrue up to 240 hours.

Methodology

To meet this objective, we:

- Interviewed the city manager and personnel director to understand the procedures regarding the authorization, approval, and payment of overtime;

- Examined federal and state laws and regulations related to overtime;

- Reviewed policies and procedures and CBA provisions related to overtime; and

- Selected a judgmental sample of departments and employees with high overtime amounts to determine compliance with policies and procedures, FLSA requirements for overtime documentation, and the state requirements for timely payment of wages.

Audit Results

Overtime

Our audit revealed that the design of Brigantine’s system of internal controls for the payment of overtime was adequate but the implementation of those controls needs to be strengthened. We identified 105 employees that received overtime payments in 2021. We judgmentally selected 16 salaried, non-exempt employees who received overtime payments, which included 5 police officers and 1 dispatcher from the police department; 5 firefighters; and 4 employees designated as laborer operator drivers and 1 supervisor from the public works department. Our testing included review of 48 timesheets. We found exceptions with the police dispatcher omitting the reason or explanation for overtime on 10 occasions covering 3 timesheets. We confirmed that reasons for overtime are required to be included on timesheets whenever overtime is worked. Once we made officials aware of the situation, the city manager held a meeting with the police chief and the dispatcher to make clear that future overtime documentation must include an explanation prior to the issuance of payment.

The personnel director utilizes a paper system for tracking the time and attendance of all employees, however, some departments maintain their own electronic time and attendance systems. During our review, we confirmed that the personnel director does not have direct access to the systems used by other departments. For example, the police department uses police scheduling software that includes a feature that does not allow overtime to be approved if a reason for the time worked has not been included. This feature is currently not being utilized. If it had been used, timesheets without a justification for overtime would not have been approved. The city manager stated the City is considering purchasing a civilian version of the software that would include the same overtime control feature. The City’s management should design its information system, including for timekeeping, and related control activities to achieve objectives and respond to risks involving overtime.[8]

Compensatory Time

We found that the City allowed the tax assessor, an exempt employee, to accrue 1,947 hours of compensatory time as of January 1, 2013. The City’s policy allows exempt employees to accrue up to 40 hours of compensatory time at the discretion of the city manager. The City made payments to this employee from 2016 through 2020 to eliminate the accrued time owed and to comply with its current policy.

Our testing also found that all five public works employees sampled carried over unused compensatory time into the subsequent year, which is prohibited by their CBA. A discussion with Brigantine found that officials were not aware of this provision in the CBA and allowed all public works employees to carry over unused compensatory time.

Nepotism

Our review found that one employee signed off on the timesheets, including overtime, of his brother. The superintendent of public works supervises his brother, a supervisor in that department, and completes his annual reviews. The anti-nepotism policy in Brigantine’s 2021 Employee Handbook does not allow immediate relatives to be employed in regular full-time positions where “one relative would have the authority to supervise, appoint, remove, discipline or evaluate the performance of the other.” The City has violated this policy.

Cause

Brigantine did not consistently follow its own policies and procedures for documenting the reasons for overtime, accruing compensatory time, and preventing nepotism.

Effect/Potential Effect

Failure to follow policies may weaken the City’s system of internal control and limit its ability to identify and prevent fraud, waste, or abuse.

Recommendations

5. Ensure that timesheets document the reasons for any overtime worked as required.

6. Adhere to the terms of the current public works CBA and cease the carryover of unused compensatory time to the subsequent year.

7. Designate a third party to attend personnel meetings, sign off on performance reviews, and approve timesheets in order to ensure compliance with the City’s anti-nepotism policy.

D. Health Benefits Administration

Objective: To determine whether the City was effectively administering and monitoring employee health benefits.

Finding

The City failed to comply with state statutes and to follow local finance notice guidance for the administration of health benefit waivers, resulting in wasteful payments of approximately $64,500.

Criteria

N.J.S.A. 40A:10-17.1 allows employees of local units to waive participation in a healthcare plan if they are eligible for other healthcare coverage and, in exchange, to receive a payment which shall not exceed 25 percent, or $5,000, whichever is less, of the amount saved. The Division of Local Government Services, within the state Department of Community Affairs, issued Local Finance Notice 2016-10 to remind local units of existing laws regarding payments made to employees who waive coverage. The finance notice advises local units that employees receiving waivers must be eligible for other coverage and strongly recommends that the governing body annually review its policies on such payments, consider the impact on municipal budgets, and determine the fiscal prudence of continued waiver payments. The finance notice also reaffirms that municipalities have sole discretion regarding whether to offer employees payment for the waiver of health benefits. This discretion also extends to the amount of the waiver payment as long as it does not exceed the maximum amounts established by the statute. Health benefit waivers are statutorily prohibited from being subject to the collective bargaining process.

Methodology

To meet this objective, we:

- Interviewed the city manager and personnel director to understand the administration of health benefits;

- Reviewed the City’s policies, statutes, regulations, and local finance notice guidance;

- Examined supporting documentation for health insurance coverage and health benefit waivers from 2019 through 2021;

- Determined employees’ eligibility for health benefits and health benefit waiver payments; and

- Recalculated waiver payments for 30 employees.

Audit Results

We found that the City did not have formal policies and procedures in place for administering health benefit waiver payments. The City should implement control activities through policies.[9] Payments in lieu of health benefits are intended to save taxpayer dollars. These payments may no longer be necessary because the avoidance of statutorily required employee contributions toward health benefits is likely alone a sufficient financial incentive to waive benefit coverage when alternative coverage through a family member is available. The intention of the statute is to generate savings for the employer by allowing waiver payments to employees who forgo employer-provided health benefits.

Under the City’s approach, if related employees are both eligible for City-provided health insurance coverage, one employee may receive payment for waiving coverage while also receiving the City’s health insurance coverage through their eligible family member. As a result, employees “double dip” and receive waiver payments while simultaneously receiving health benefits from the City, which causes additional wasteful costs to taxpayers. From 2019 through 2021, 55 City employees received approximately $542,000 in waiver payments. Six of those employees were covered by City-provided health insurance through a family member and also received approximately $64,300 in waiver payments. Brigantine should eliminate these wasteful waiver payments to employees who receive coverage from the City as this is a duplication of benefits.

Additionally, our review identified an employee receiving a waiver payment in excess of the established cap. Waiver payments made after May 21, 2010 may not exceed 25 percent of the amount saved, or $5,000, whichever is less. Contrary to the law, the employee received a waiver payment of approximately $5,200 in 2020.

Cause

Brigantine does not have a policy prohibiting health benefit waiver payments to those receiving City-provided health insurance coverage through a family member and did not comply with N.J.S.A. 40A:10-17.1.

Effect/Potential Effect

The City allowed an overpayment of $200 and made wasteful health benefit waiver payments of approximately $64,300 to employees receiving City-provided health insurance through a family member.

Recommendation

8. Eliminate waiver payments to employees receiving City-provided health insurance through a family member.

9. Develop policies and procedures for administering health benefit waivers. The policy should require an annual review to ensure that waiver payments comply with the law and remain fiscally prudent. The City should evaluate whether the requirement that employees contribute to the cost of their health insurance obviates the need for employees to receive waiver payments. If the waivers are found to no longer be beneficial, the City should reduce or eliminate the payments accordingly.

E. Health Benefit Plan Cost Savings

Objective: To determine whether the City could have saved money by joining the State Health Benefits Program (SHBP).

Finding

The City’s failure to substantiate 2021 rate information and assumptions in its health insurance broker’s cost analysis resulted in the potential loss of $191,000 in healthcare savings.

Criteria

Waste is described as the act of using or expending resources carelessly, extravagantly, or to no purpose. Importantly, waste can include activities that do not include abuse and does not necessarily involve a violation of law. Rather, waste relates primarily to mismanagement, inappropriate actions, and inadequate oversight.[10]

Management should evaluate external information received against the characteristics of quality information and information processing objectives and take any necessary actions so that the information is quality information. Quality information is appropriate, current, complete, and accurate.[11]

Methodology

To meet this objective, we:

- Interviewed the city manager and personnel director to understand health benefit administration and procurement;

- Reviewed CBA terms regarding health benefit coverage; and

- Reviewed the health insurance broker’s health insurance cost analyses for 2019 through 2021.

Audit Results

The City obtains new health insurance coverage annually through a health insurance broker. The broker presents cost comparisons for several medical and prescription plans, including the SHBP. City officials review the presentation and present their choice of healthcare coverage to the Council for approval. Our review identified discrepancies within the 2019, 2020, and 2021 broker’s analyses that included omission of relevant rate plans, use of inaccurate rates, exclusion of applicable contributions, and unsubstantiated medical waiver payment assumptions. We evaluated the effects of these discrepancies in the broker’s 2021 analysis.

Direct 15 Rate Plan Omission

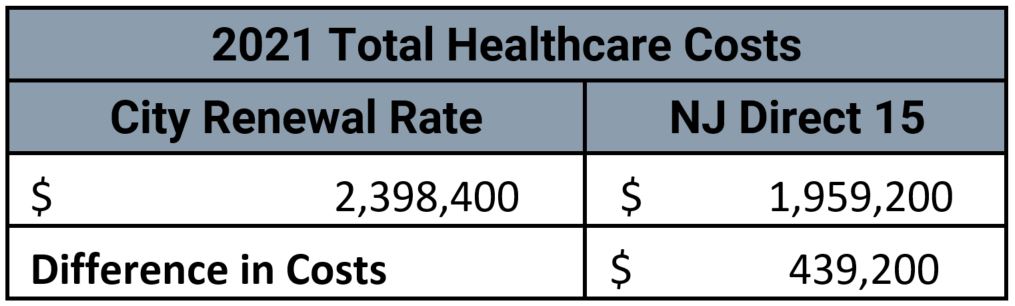

Brigantine’s CBAs require the City’s health insurance plan to be equivalent to the SHBP DIRECT 10 (Direct 10) plan. All CBAs, except those covering fire department employees, allow covered members to move to the SHBP Direct 15 (Direct 15) equivalent plan in the event that the City moves to the Direct 15 equivalent plan. Historically, the Direct 15 plan has been less expensive than the Direct 10 plan. However, we noted that the broker only included Direct 15 as part of its analysis in 2020 and excluded the plan entirely in both the 2019 and 2021 analyses. Although not within our scope, we found the broker’s presentation for 2022 also excluded plan coverage cost options for Direct 15. Based on the provisions in the CBAs, the City should require the broker to include the less expensive NJ Direct 15 rates in its analyses. Our review found the 2021 Direct 15 total healthcare costs[12] to be substantially cheaper than the City’s renewal rates by approximately $439,200 as seen in the chart below. As a result, we conclude that the broker’s presentations lacked all relevant plan options for City officials to make an unbiased decision for the most cost-efficient health insurance plan.

Inaccurate Rates

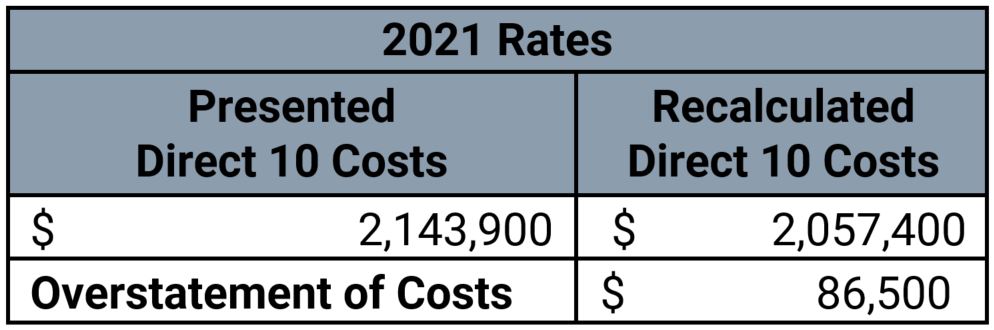

The broker’s 2019 and 2021 analyses also used rates that did not reflect the cost of buying medical and prescription coverage together at a discount. Instead, the broker used rates that were for medical and prescription coverage purchased separately and at full cost. When we applied the discounted rates in our own 2021 cost evaluation, we found the inaccurate rates overstated the estimated total medical costs for Direct 10 by approximately $86,500. The chart below illustrates the difference in costs between the rates presented by the broker and the recalculated costs using the discounted rates for the Direct 10 Plan.

Exclusion of Applicable Contributions

The broker's 2021 analysis estimated employee contributions toward the cost of City-provided dental and vision coverage of approximately $51,000. The broker deducted employee dental and vision contributions from the estimated costs associated with the City’s current plan offerings but did not deduct the contributions from the estimated costs of the SHBP plan offerings. The explanation provided by the broker was that the New Jersey statute excludes dental and vision contributions from the SHBP plans. However, the employees’ share of the cost of dental and vision coverage are separate from the contributions required for employee medical benefits and are established by a CBA, ordinance, or resolution. A change in the medical insurance provider would not eliminate the dental and vision contribution requirement for employees altogether, but rather require that the contribution amounts be set by the employee’s CBA, or by an ordinance or resolution for those employees not covered under a CBA. As a result, the broker’s 2021 analysis overstated the Direct 10 costs by approximately $51,000 by speculating on a change to employee contributions that may not occur.

Unsubstantiated Medical Waiver Payment Assumptions

The broker’s presentation included assumptions regarding the number of employees who would choose the City’s health plan if the City enrolled in the SHBP. Employees who have SHBP insurance coverage through a family member may not receive payment for waiving SHBP insurance coverage from their employer. An employee’s costs for insurance coverage increase with their salary. This and the lack of waiver payments incentivize employees to obtain their SHBP insurance coverage through the family member with the lowest salary in order to decrease the cost of insurance coverage to the family as a whole. As mentioned previously, waiver payments in lieu of health benefits are intended to save money by reducing costs.

The broker’s 2021 analysis estimated that there would be 42 employees receiving insurance waiver payments from the City, including 32 who had the SHBP as their alternate plan. The broker presented two scenarios in which either 18 or 25 employees would choose the City-provided insurance coverage since these employees would no longer be eligible for a waiver payment. The presentation identified the additional costs to the City if these employees chose to enroll in the SHBP medical benefits provided by the City.

We performed an evaluation of employees receiving health benefit waivers to determine if the broker’s assumptions were reasonable. We identified 47 employees who received waiver payments in 2021. Of the 47, we identified 31 as having state health coverage as their alternative coverage. We performed an analysis to determine the number of waiver recipients with a financial incentive to switch to health benefits offered by the City. Our analysis identified seven City employees whose salaries were lower than that of the family member providing alternate coverage through the SHBP and who would likely switch to health insurance coverage provided by the City. It is unlikely that the remaining 24 employees would choose the City plan and contribute more to obtain the same coverage they currently have. While it is plausible that enrolling in the SHBP would encourage some employees to opt into the City’s plan, that number was likely significantly lower than estimated by the broker.

Potential Savings

The 2021 broker’s analysis, which only included the Direct 10 plan, estimated that switching to the SHBP would cost the City between approximately $234,000 and $395,000 if 18 or 25 employees currently receiving medical waiver payments opted into the City’s health plan, respectively. When we recalculated the plan offerings with accurate rates, employee contributions for dental and vision coverage for all plans, considered potential dividends, and assumed only seven employees waiving coverage would choose City-provided SHBP coverage, we estimated that the City could have potentially saved approximately $116,000 by joining the Direct 10 plan. Furthermore, a similar analysis considering the Direct 15 plan rates identified potential savings of approximately $191,000.

As part of its service to the City, the broker makes suggestions regarding health plan options based on costs and potential savings. As recognized by the Division of Local Government Services’ 2021 best practices, such an arrangement results in conflicting incentives that may harm a municipality.[13] The broker receives commissions directly from the insurance companies based on a percentage of medical and prescription healthcare coverage costs, as well as the number of monthly enrollees for dental and vision coverage, rather than a flat fee rate. This creates an inherent conflict between the broker and City officials seeking the most cost-efficient insurance coverage.

Based on the discrepancies mentioned above, we found the City did not confirm information provided by the health insurance broker or reevaluate costs independently based upon reliable information. The City’s management should be evaluating information it receives from external sources to ensure it is relevant and reliable.[14] The broker does not earn a commission if the City participates in the SHBP. It is, therefore, extremely important that the City independently review the information provided by the broker to ensure it is accurate, relevant, and presented in an unbiased manner. Municipalities must ensure transparency during the healthcare selection process and not simply defer to a person with a financial self-interest in persuading the City to not use the SHBP.

Cause

The City relied on the health insurance broker’s analyses of health insurance costs without verifying that the information provided by the broker was accurate and relevant.

Effect/Potential Effect

The City did not properly evaluate the data received from its broker when making its selection for 2021 healthcare coverage. The City did not realize potential savings under the SHBP Direct 10 and Direct 15 plans of approximately $116,000 and $191,000, respectively.

Recommendations

- Substantiate the data received by the insurance broker to ensure the analysis includes accurate and relevant data concerning rates, employee contributions, and employee health benefit waivers. Request that the broker provide support for its analysis.

- Agree upon a flat fee rate, not to exceed the contract amount for insurance broker services, instead of a commission-based payment to mitigate the risk of the broker recommending more expensive health insurance coverage in order to increase its commissions. The flat fee rate should be the only compensation provided to the broker by the City or insurance provider. Any additional compensation received by the broker should be returned to the City or credited to the insurance premiums.

- Seek advice from legal counsel to determine if the broker-supplied information and recommendations for insurance plan selection met all contractual, legal, and ethical obligations for 2019, 2020, and 2021. To the extent legal counsel’s review reveals any deficiencies, determine whether the City should pursue an appropriate legal remedy.

F. Lifeguard Pension Plan

Objective: To determine whether the City was effectively administering its lifeguard pension plan.

Finding

The City’s contributions to the lifeguard pension plan (Plan) were less than required in 2020 and 2021. The Plan does not allow employees to withdraw their contributions upon separation of employment.

Actuarial calculations of the Plan’s liabilities were not current and Plan financial statement disclosures did not meet Governmental Accounting Standards Board (GASB) requirements in 2019 and 2020. A recently obtained actuarial report disclosed an unfunded accrued liability of $4.5 million.

Criteria

New Jersey law requires cities bordering the Atlantic Ocean to provide pensions to lifeguards who serve for twenty years upon reaching the age of forty-five. Municipalities incorporated as towns, townships, or boroughs that border the Atlantic Ocean are not subject to this requirement. Brigantine has a Plan that provides eligible members an annual amount equal to 50 percent of the average of their three highest years’ earnings. The City maintains a trust fund for the purpose of making payments and accumulating contributions. The employee and the City must each contribute four percent of the employee’s annual salary to the fund. Funds in excess of the required contributions must be included in the City’s tax levy. The Plan and related statutes do not require the return of employee contributions. The City’s annual audit reports on balances and financial activity related to the Plan. GASB issued Statement 73 to improve the usefulness of information about pensions included in financial reports of state and local governments.[15] GASB Statement 73 requires, among other things, the use of recent actuarial reports to determine the employer’s total pension liability and the disclosure of that liability.

Methodology

To meet this objective, we:

- Interviewed personnel responsible for finance and administration;

- Reviewed Plan documents, actuarial reports, and supporting documentation;

- Reviewed statutes, regulations, GASB statements; and

- Documented City compliance with state statutes and GASB statements.

Audit Results

Contributions

We reviewed Plan contribution information provided by the City. The City is required under the Plan and N.J.S.A. 43:13-27(b) to contribute an amount equal to the four percent employee contribution. The contribution data we reviewed indicated that employee contributions exceeded employer contributions for 2020 and 2021. City records indicate that since 1990 employee contributions exceeded employer contributions in 21 of the last 32 years, with employee contributions exceeding the City’s contribution and interest earnings by approximately $113,300.

Brigantine’s Plan does not require the City to provide for the return of contributions to employees upon separation of employment prior to 20 years of service. The lack of a mechanism to return employee-provided contributions provides an inequitable benefit to the City and those employees who are able to provide 20 years of service in a seasonal position to the detriment of those who cannot.

GASB Requirements

We obtained an actuarial report for the Plan dated December 31, 2005. GASB 73 requires actuarial valuation to be conducted no more than 30 months and one day earlier than the employer’s most recent fiscal year-end. The City did not comply with this requirement until recently. This reduces management’s ability to identify and anticipate the potential budgetary effects of the Plan’s provisions. During the course of our audit, the City obtained an updated actuarial report for the Plan that will allow disclosure of the fund liability in its current annual audit. The report indicates that the Plan has an unfunded accrued liability of $4.5 million and recommends increasing the annual contribution to $358,000. The City’s annual contribution for 2019 through 2021 was $20,000.

Cause

Management did not obtain periodic actuarial reports and did not make the required Plan contributions. State law does not require the Plan to allow for the withdrawal of employee contributions upon separation from employment prior to vesting.

Effect/Potential Effect

The most recent actuarial report indicates an unfunded accrued liability of $4.5 million. The City will have to increase its appropriation to the lifeguard pension trust fund to pay the liability over time. In addition, the inability of lifeguards to get their contributions returned at separation of employment creates an unfair benefit to the City.

Recommendation

- Increase City contributions to the Plan by tax levy to ensure that City contributions, at minimum, comply with the requirements of N.J.S.A. 43:13-27(b) and address the unfunded liability noted in the actuarial report.

- Comply with GASB 73 financial statement disclosure requirements regarding the Plan.

- Seek advice from counsel regarding an amendment to the Plan allowing employees to withdraw contributions upon separation of employment.

Reporting Requirements

We provided a draft copy of this report to Brigantine officials for their review and comment. The City generally agreed with our audit findings and conclusions, and its response indicated the City has taken steps and will continue to implement corrective actions to address our recommendations. Brigantine’s comments were considered in preparing our final report and are attached as Appendix A.

We are required by statute to monitor the implementation of our recommendations. In accordance with N.J.A.C. 17:44-2.8(a), within 90 days following the distribution of the final audit report, the City is required to provide a plan detailing the corrective action taken or underway to implement the recommendations contained in the report and, if not implemented, the reason therefore. We will review the corrective action plan to evaluate whether the steps taken by the City effectively implement our recommendations.

We thank the management and staff of Brigantine for the courtesies and cooperation extended to our auditors during this engagement.

Footnotes

[1]https://www.gao.gov/assets/gao-21-368g.pdf.

[2] UNITED STATES GOVERNMENT ACCOUNTABILITY OFFICE, STANDARDS FOR INTERNAL CONTROL IN THE FEDERAL GOVERNMENT (SEPT. 2014) (“Green Book”), https://www.gao.gov/assets/gao-14-704g.pdf.

[3] S. 4, 214th Leg. (N.J. 2010), (“2010 law”), https://www.njleg.state.nj.us/2010/Bills/AL10/3_.HTM.

[4] STATE OF N.J. OFFICE OF THE STATE COMPTROLLER, A REVIEW OF SICK AND VACATION LEAVE POLICIES IN NEW JERSEY MUNICIPALITIES, 13-14 (July 2022), (“Sick and Vacation Leave Report”) https://www.nj.gov/comptroller/news/docs/sick_leave_report.pdf.

[5] STATE OF N.J. OFFICE OF THE STATE COMPTROLLER, Sick and Vacation Leave Report at 16.

[6] FAIR LABOR STANDARDS ACT, 29 U.S.C. § 201 et al, see also 29 C.F.R. 553, (“FLSA”).

[7] https://www.dol.gov/agencies/whd/fact-sheets/17a-overtime.

[8] U.S. GOVERNMENT ACCOUNTABILITY OFFICE, Green Book at 9.

[9] U.S. GOVERNMENT ACCOUNTABILITY OFFICE, Green Book at 9.

[10] U.S. GOVERNMENT ACCOUNTABILITY OFFICE, GAGAS at 114.

[11] U.S. Government Accountability Office, Green Book at 62, 60.

[12] Total healthcare costs are the initial costs calculated prior to any other considerations (e.g., contributions or discounts).

[13] NJ Division of Local Government Services, 2021 Best Practices Inventory (2021), https://www.nj.gov/dca/divisions/dlgs/programs/best_practices_docs/2021%20DLGS%20Best%20Practices%20Inventory%20Questions%20.xlsx at Question 10 (“Insurance broker fees dependent on the amount of health insurance premiums or fees paid by the municipality are vulnerable to abuse as brokers could face conflicting incentives in seeking lower-cost health insurance alternatives.”).

[14] U.S. Government Accountability Office, Green Book at 59.

[15] GOVERNMENTAL ACCOUNTING STANDARDS BOARD, STATEMENT NO. 73, “ACCOUNTING AND FINANCIAL REPORTING FOR PENSIONS AND RELATED ASSETS THAT ARE NOT WITHIN THE SCOPE OF GASB STATEMENT 68 AND AMENDMENTS TO CERTAIN PROVISIONS OF GASB 67 AND 68” (June 2015), https://gasb.org/.

Press Contact

Pamela Kruger

Pamela.Kruger@osc.nj.gov

609-789-5094

Waste or Abuse

Report Fraud

Waste or Abuse