Official Site of The State of New Jersey

Official Site of The State of New JerseyTax Credit Use Cases

Example Use Case 1: School District

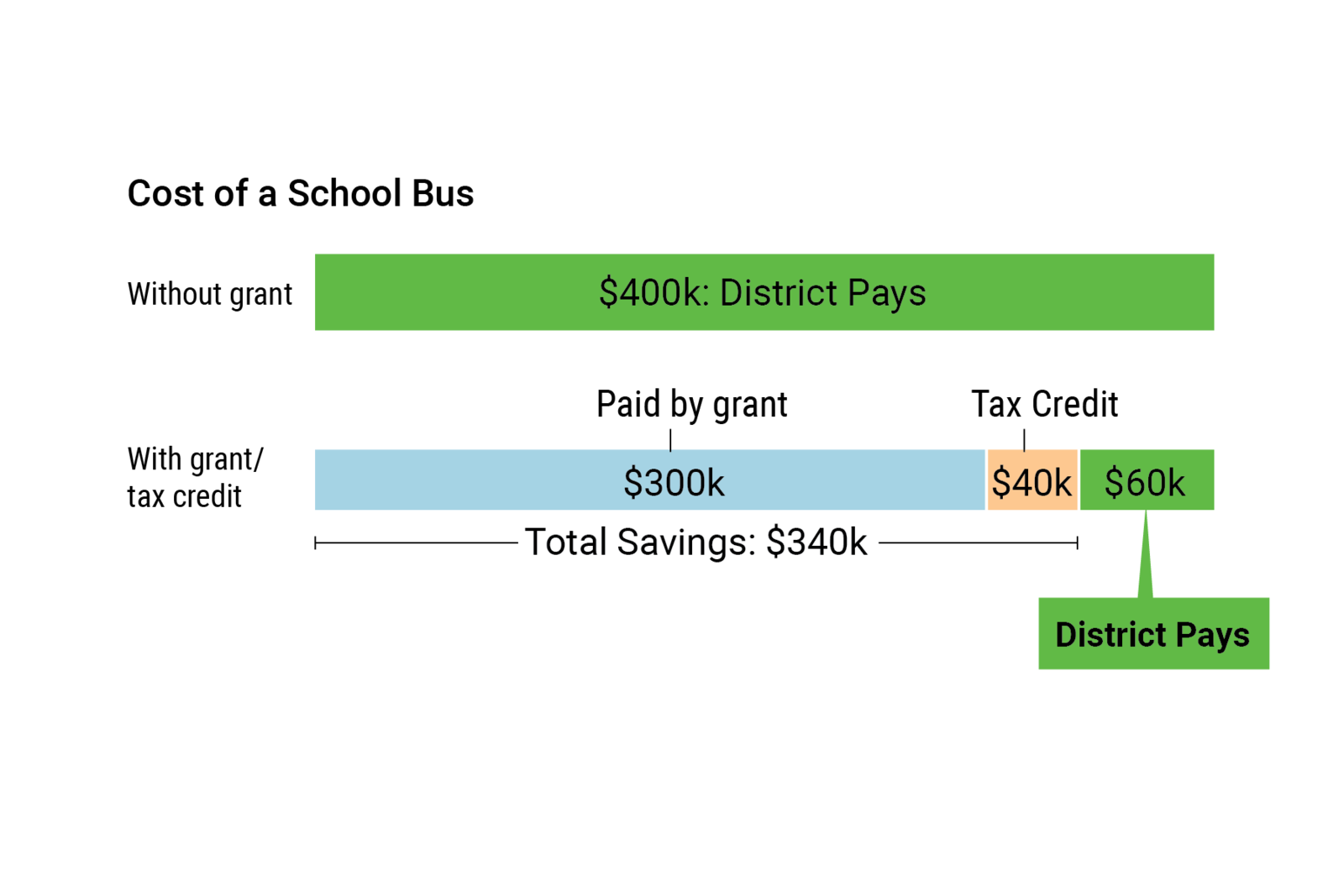

A public school district purchases an electric school bus to replace an older diesel-fueled bus in its fleet. The cost of the bus is $400,000. Under IRA, clean commercial vehicles are eligible for a maximum tax credit of up to $40,000 per vehicle.

While the district could file solely for “Direct Pay,” in this example the district chose to apply for a grant as well. The district wanted to combine the grant AND the value of the tax credit direct payment toward the purchase price.

The grant application was successful, and the district was awarded $300,000 toward the purchase of the bus. Therefore, the district’s original $400,000 cost for the bus is reduced $300,000 by the grant and $40,000 by the tax credit for a total cost reduction of $340,000. By combining the grant and the tax credit, the district pays only $60,000 of the $400,000 total cost.

Please note, the cost of the tax-exempt grant plus the IRA tax credit cannot be more than the cost of the bus.

IRA Direct Pay Tax Credit Program: Credit for Qualified Commercial Clean Vehicles

Breakdown

Example Use Case 2: Public Universities

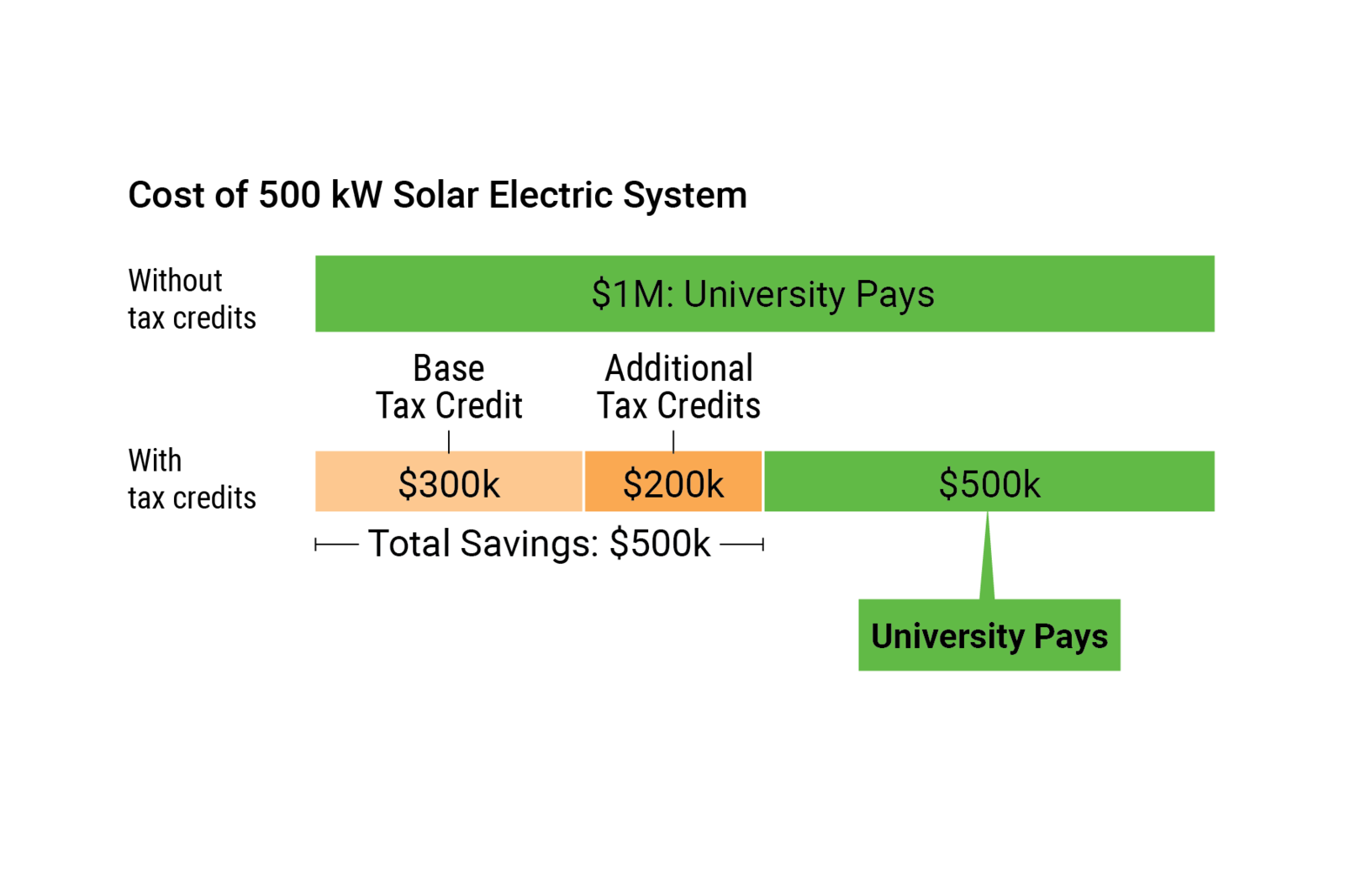

1. A public university wants to invest in a project to increase electricity production capacity. It investigates a variety of options and decides to purchase and install a 500 kW solar electric system at a cost of $1 million. This investment would qualify for a base credit of 6% and meets all apprenticeship and prevailing wage requirements which brings the credit up to 30% or $300,000. However, since the project is located in an energy community and it meets domestic content requirements (used a sufficient share of materials produced in the U.S.), it is eligible to receive two additional credits of 10% each, which in this case have a combined total of $200,000. The tax credit would then be $500,000 or half of the system’s cost. In addition, if the system provides electricity beyond the facilities immediate needs, the “excess” power generated may offset existing costs for other parts of the university.

IRA Direct Pay Tax Credit Program(s): Investment Tax Credit for Energy Property and Low-Income Communities Bonus Credit

$1,000,000 cost less $300,000 (base + apprenticeship + prevailing wage requirements) less $100,000 for domestic content credit and $100,000 low-income community bonus credit = $500,000 final cost

2. In another example, a university implements a project to rehab a 100,000 square foot building. The school hires a contractor to install new lighting, insulation, and system controls that will increase the building’s energy efficiency by 25%. Throughout construction, the contractor meets federal apprenticeship and prevailing wage requirements that makes the project eligible to receive a tax credit payment of $250,000 ($2.50 x 100,000 sq ft). This tax credit payment decreases the overall cost of the project that benefits university staff, faculty, student body and community.

IRA Direct Pay Tax Credit Program: Energy Efficient Commercial Buildings Deduction

Breakdown

Example Use Case 3: Regional Hospital Campus Microgrid

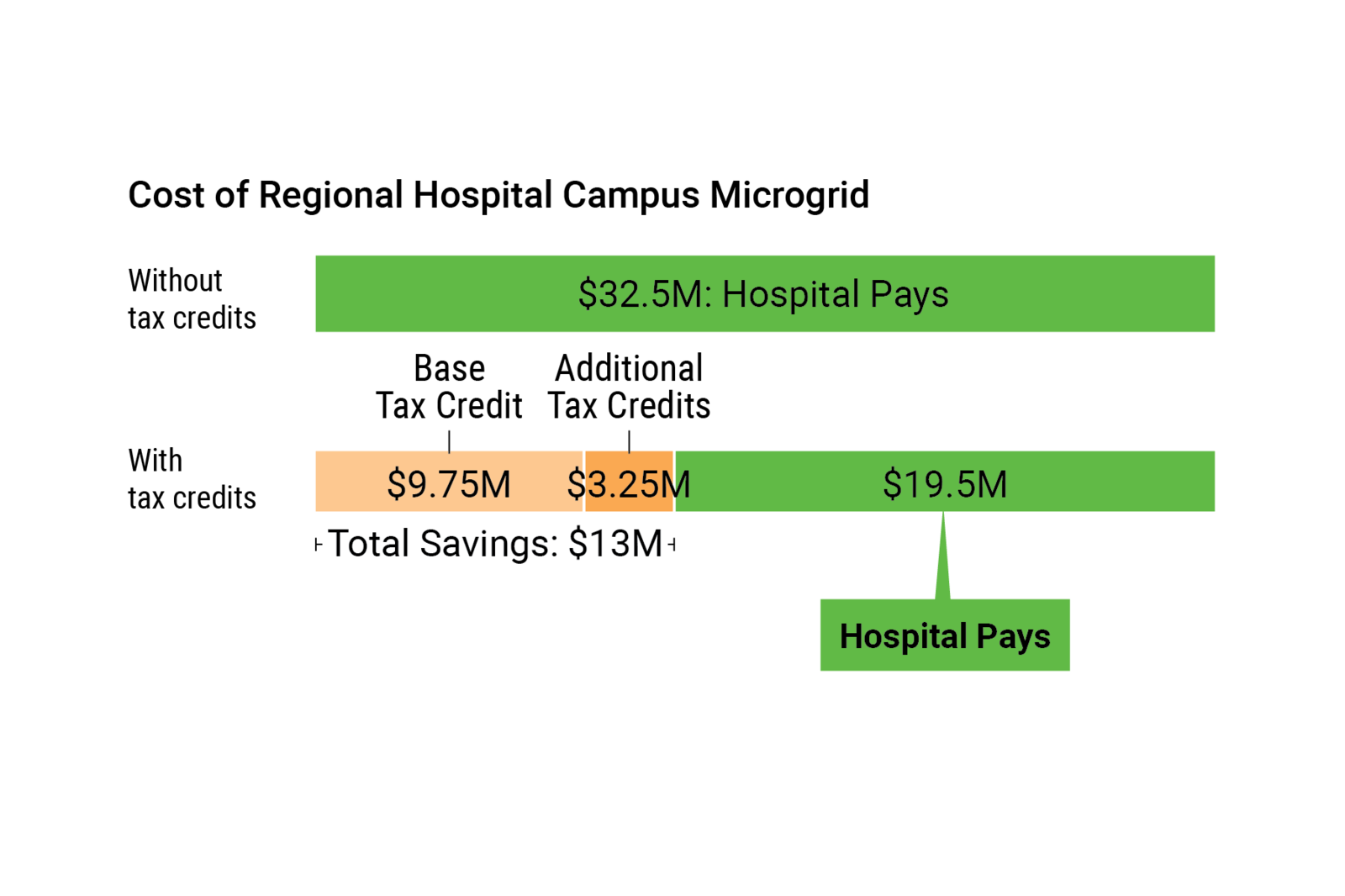

A regional hospital campus serving an Overburdened Community wants to install a renewable energy microgrid to begin operation in 2025. The microgrid, comprised of a 1.32 MW solar PV, a 2.2 MW fuel cell, and a 1.4 MWh battery, will ensure the hospital and its campus remain operational during regional power outages. This project will reduce the hospital’s reliance on the traditional power grid, mitigate power interruptions, and reduce building/campus emissions. Currently, the hospital depends on an aging substation transformer and emergency diesel generators to remain operational and deliver healthcare services during power disruptions. The new microgrid will power both normal operations and emergency services with sustainable energy sources, meeting 80% of the hospital’s peak time energy needs.

Prior to the passage of the Inflation Reduction Act of 2022 (IRA), this renewable energy microgrid project was cost prohibitive, however, by using IRA tax credits the project's cost feasibility improved allowing the project to move forward.

By leveraging these IRA funding mechanisms, the project will receive approximately $13 million in tax credit direct payments, which will cover about 40% of the initial capital outlay.

IRA Direct Pay Tax Credit Program(s): Investment Tax Credit for Energy Property with Domestic Content Bonus Credit and Low-Income Communities Bonus Credit.

Breakdown

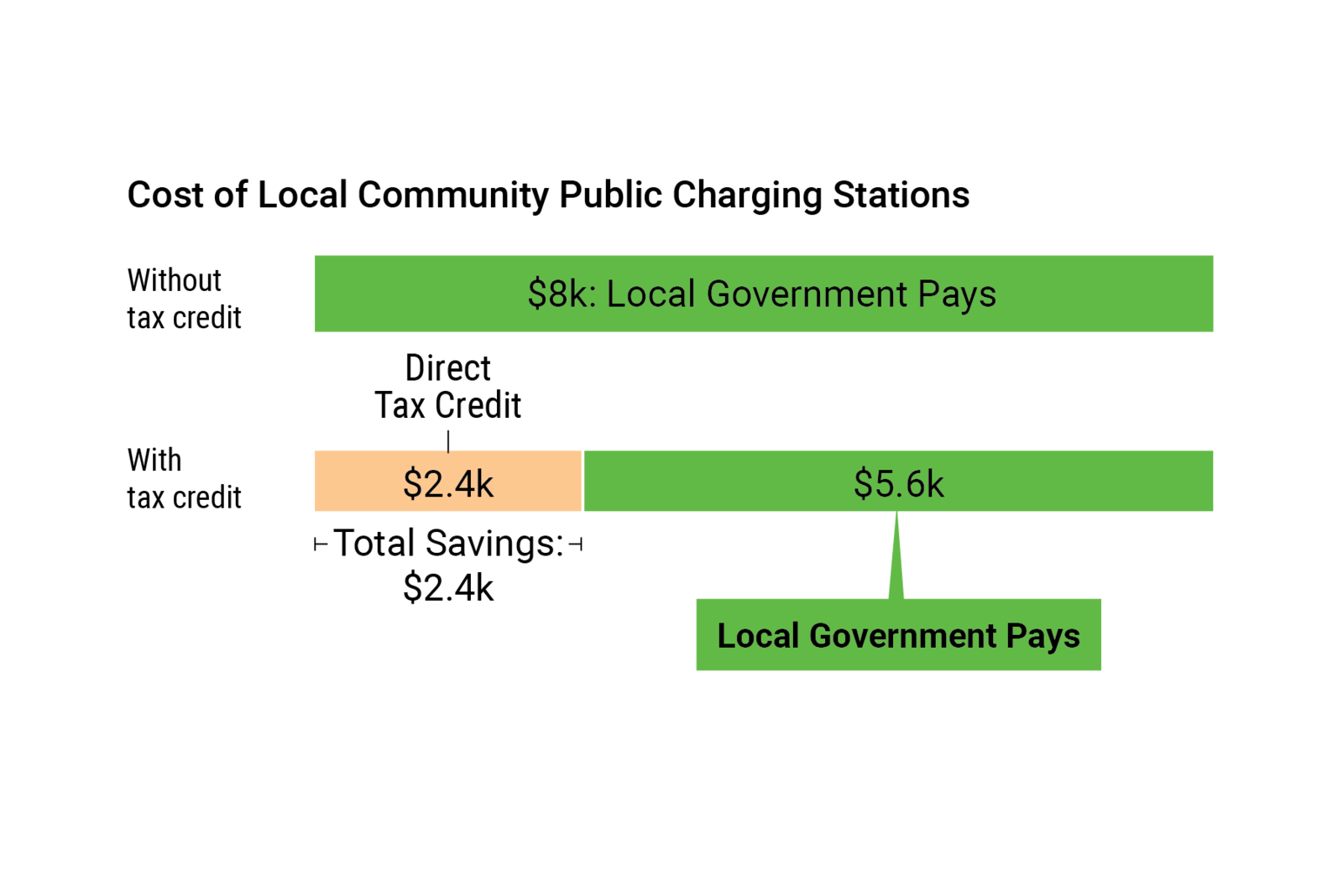

Example Use Case 4: Local Community Public Charging Stations

A local government has installed two Level-2 electric vehicle (EV) charging stations at its City Hall/Community Center which allow four vehicles to charge at once. The stations will provide fleet charging infrastructure for government light duty vehicles, facilitating the transition to a low/zero emissions municipal fleet which will save operational dollars and result in health benefits from zero tailpipe emissions. In addition to saving taxpayer dollars and demonstrating the City's commitment to sustainability, the community directly benefits from the EV charging infrastructure as the public is allowed to charge their EVs at no cost during the day while local government vehicles are out in the field.

The City qualifies for a direct tax credit as the project is located in a low income or rural census tract and anticipates receiving a payment equal to 30% of the cost of the refueling property.

IRA Direct Pay Tax Credit Program: Alternative Fuel Vehicle Refueling Property Credit.

Breakdown