Official Site of The State of New Jersey

Official Site of The State of New Jersey

Report on COVID-19 CARES Act Marine Fisheries Assistance Grant Program

Table of Contents

- Posted on - 03/24/2022

Introduction

Pursuant to Executive Order 166 (Murphy), N.J.S.A. 52:15C-1 to -24, and N.J.S.A. 52:15B-1 to -16, the Office of the State Comptroller (OSC) is authorized to review expenditures of COVID-19 recovery funds for issues of potential fraud, waste, and abuse. OSC conducted a limited review of the New Jersey COVID-19 CARES Act Marine Fisheries Assistance Grant Program (program or Fishery Program) administered by the New Jersey Department of Environmental Protection (DEP). OSC evaluated whether DEP took appropriate steps to prevent and detect fraud, waste, abuse, and improper payments in its administration of the program; whether program recipients disclosed other sources of COVID-19 assistance received, as required by the Fishery Program guidelines; whether program recipients had been made “more than whole” by their receipt of assistance from the Fishery Program; and whether program recipients had accurately documented their annual revenue and March to June revenue for the period 2015 to 2020.

Based on a review of a judgmental sample of 24 program recipients, OSC found the following:

- DEP failed to address red flags in applications, which led to approximately $240,000 in improper payments.

- At least nine recipients did not disclose other sources of COVID-19 assistance in their applications.

- Ten recipients were made “more than whole,” e. they received assistance that more than covered their revenue losses for 2020. Those ten program recipients received almost $2.4 million that, according to Fishery Program guidelines, should be returned.

- Eight recipients reported revenue figures that were not supported by their documentation. Several recipients failed to provide the documentation necessary for OSC to complete a full analysis.

Overall, OSC found that DEP acted in accordance with federal guidance, which prioritized the rapid distribution of funding and allowed for self-certifications and self-reporting. But quick payments should not have been the only goal; DEP was also required to take reasonable steps to mitigate the risk of fraud, waste, and abuse. In DEP’s efforts to distribute funds quickly, it failed to take steps to address red flags that would have added little to no time to the process, but would have reduced the risk of fraud, waste, abuse, and improper payments in the program.

OSC recommends that DEP review these findings to determine appropriate next steps, including recoupment and return of excess funds to the Atlantic States Marine Fishery Commission (ASMFC), or, if allowable, reallocation of the funds to other eligible recipients and/or purposes.

Background

On May 7, 2020, the United States Secretary of Commerce announced the allocation of $300 million in fisheries assistance funding. These funds were provided by Section 12005 of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act). New Jersey received approximately $11.2 million in funding for marine fishery industries that were impacted by closures caused by the COVID-19 pandemic.[1]

The funds were intended to be distributed quickly. Both the CARES Act itself and implementation guidance from the federal Office of Management and Budget (OMB), OMB Memo 20-21, indicated the importance of disbursing the funding quickly to those in need of assistance. OMB Memo 20-21 also directed agencies to strike a balance between expediency and good stewardship and to prioritize transparency and accountability to help safeguard taxpayer dollars.[2]

The funding was distributed to the State through the National Oceanic and Atmospheric Administration Fisheries (NOAA) and its partner, the ASMFC. Pursuant to Section 12005 of the CARES Act, fisheries and other fishing-related businesses were eligible to seek relief funding to cover revenue losses if they suffered, as a direct or indirect result of the COVID-19 pandemic, a greater than 35 percent loss in revenue compared to their prior five-year average. The ASMFC worked with the State to develop a Spending Plan consistent with the CARES Act and NOAA guidance (Spending Plan). New Jersey’s Spending Plan was approved by NOAA and included information addressing program eligibility, loss and payment calculations, the self-certification process, and the review and appeals process.

DEP was responsible for the administration of the application and distribution process for the Fishery Program in accordance with its Spending Plan. Applicants were instructed to utilize DEP’s online portal, System for Administering Grants Electronically (SAGE), to submit their applications. The portal included a link for “further guidance,” which linked to a “Funding Notice” that largely mirrored the Spending Plan. The public website for the program also included a Frequently Asked Questions (FAQ) document that addressed eligibility, eligible losses, the application process, self-certifications, and payment, among other things. The Spending Plan, Funding Notice, and FAQs will be referred to hereinafter collectively as the “program guidelines.”

According to the program guidelines, to be eligible for assistance, applicants were required to, in part, certify that they had incurred a greater than 35 percent loss in fishery-related revenue between the four-month period of March 1, 2020 to June 30, 2020, as compared to their average revenue from 2015 to 2019 for the same four-month time period. Assistance was available for businesses in the following designated sectors: commercial/aquaculture, recreational, and processors/dealers.[3]

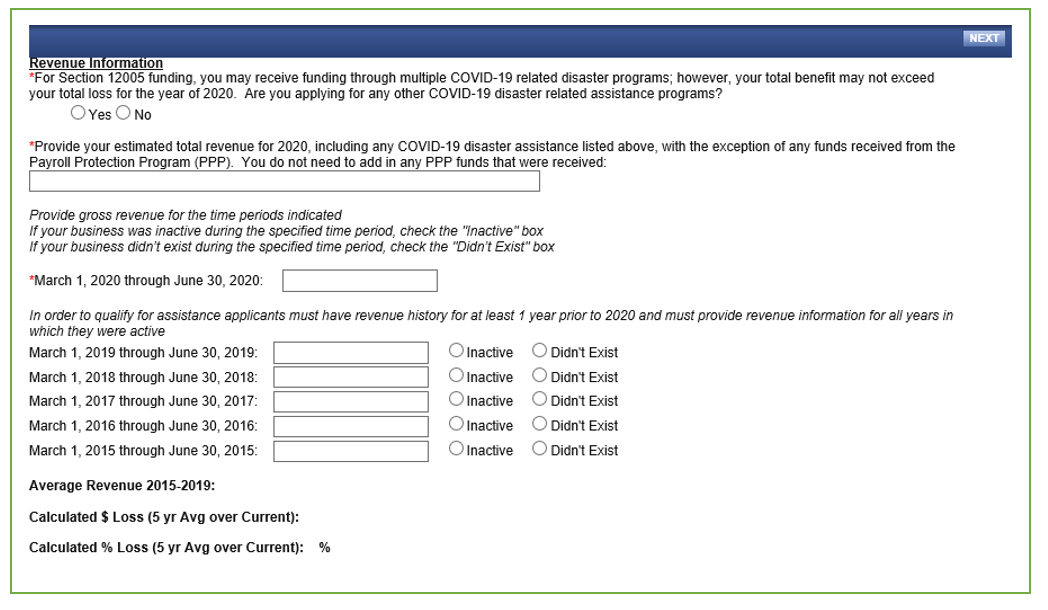

As part of the application, applicants were also required to estimate their annual revenue for 2020 and to identify any other COVID-19 disaster-related assistance they had received (other COVID assistance). Funding received, or applied for, through the U.S. Small Business Administration’s Payroll Protection Program (PPP) was required to be identified in the application, but was not required to be included in calculations of 2020 annual revenue unless the requirement to repay the funding had been forgiven. Figure 1 below shows the revenue information required by the application.

Figure 1

The program guidelines and application stated that applicants could not be made “more than whole.” That is, an applicant could not receive a total combined benefit that exceeded its total loss, inclusive of DEP assistance and any other COVID-19 assistance received. If an applicant found that it had been made “more than whole,” when comparing its 2020 total revenue to its five-year average revenue from 2015 to 2019, the program guidelines stated that the excess funds must be returned to the ASMFC. The FAQs made clear that applicants were “solely responsible for determining if they have been made more than whole.” The FAQs also provided that if an applicant refused to provide documented proof or was found to have knowingly acted in bad faith and provided falsified or inaccurate information, the applicant would be denied assistance or would be required to pay back in full all funding and be subject to penalties.

Applicants were not required to submit documents to support their stated revenue amounts but were required to execute an affidavit that included various self-certifications and assurances made by the applicant (Affidavit). By signing the Affidavit, the applicant certified, among other things, that the information was accurate, truthful, and correct. The applicant was also required to certify that it had documentation to support the losses it recorded on the application form. See Exhibit A for a Sample Affidavit.

Applications were accepted for the Fishery Program beginning in October 2020. In total, DEP awarded payments in Round 1 of the Fishery Program to 90 applicants in the amount of $10,828,963. Applicants in the “recreational” and “processor/dealer” sector were funded at 100 percent of their losses; those in the “commercial/aquaculture” sector were funded at approximately 80 percent of their losses. One of the 90 applicants returned funding after determining it had been made “more than whole,” resulting in a total of $10,824,619 distributed to 89 applicants.

Methodology

OSC’s review was limited to Round 1 of the Fishery Program. Based on an initial review of program recipients’ application information and publicly-available PPP data, OSC selected a judgmental sample of twenty-four program recipients for further review (recipients or Selected Recipients). OSC requested that DEP contact the Selected Recipients to obtain documentation to support the revenue information provided in their applications. See Figure 1 above. OSC also requested that DEP obtain documents to support the Selected Recipients’ annual revenue for the years 2015 to 2020. Applicants were not required to provide their annual revenue for 2015 to 2019 on their application forms, but this information was necessary for determining whether a recipient had been made “more than whole.”

OSC reviewed the supporting documents provided by the Selected Recipients, their applications, and publicly-available PPP data to determine whether revenue numbers were supported and whether any recipients had been made “more than whole.”

Findings

A. DEP Did Not Address Red Flags in Applications

OSC found several cases in its sample in which DEP accepted the applicant’s self-certification of its revenue loss, even when red flags were apparent. This led to ineligible recipients receiving awards and to recipients receiving excessive awards, which together total approximately $240,000 in improper payments.

The red flags included the following:

- Round numbers: Three of the Selected Recipients appeared to use estimated numbers rather than actual numbers when reporting their March to June revenue for 2015 to 2020. See Chart 1 for an example. DEP should have recognized the round figure amounts in the application and requested additional information. This recipient received an award of $37,000 ($49,000 minus $12,000) based on its reported revenue loss. In fact, the recipient had actual 2020 March to June revenue of $73,431 rather than the reported $12,000. If DEP had reviewed this recipient’s documentation in response to the presence of the red flag, it would have found that, in 2020, this applicant had actually exceeded its four-month average by almost $30,000 and, therefore, would not have been eligible for any assistance from the Fishery Program.

Chart 1: Applicant’s March to June Revenue

|

|

2015 |

2016 |

2017 |

2018 |

2019 |

2015 to 2019 Average |

2020 |

|

Reported |

- |

- |

$35,000 |

$52,000 |

$60,000 |

$49,000 |

$12,000 |

|

Actual |

- |

- |

- |

$19,386 |

$68,512 |

$43,949 |

$73,431 |

- Round numbers and identical information: Another Selected Recipient reported the exact same rounded revenue amount of $19,200 for March to June for each consecutive year from 2015 to 2019. DEP should have recognized that it is unlikely for any business to have the exact same round number revenue in 2015, 2016, 2017, 2018, and 2019. DEP should have requested additional information.

This recipient received an award of $19,200 based on its reported figures. If DEP had questioned this recipient, it would have found that the recipient did not have documentation to support these numbers, and its application presumably would have been denied. Moreover, OSC’s review of the recipient’s annual revenue figures found that the recipient did not suffer a 2020 revenue loss – its 2020 revenue exceeded its five-year average by approximately $10,000.

- Duplicate information: One Selected Recipient submitted two applications for assistance for two different business sectors, using the exact same total revenue numbers for both applications. As a result, DEP calculated the recipient’s total loss as $376,541 instead of $188,270. This recipient should not have been eligible to receive two awards based on one reported loss. If DEP had a control in place to identify the duplicate information, DEP would have avoided what appears to be an improper payment.

Through the exercise of minimal due diligence, DEP could have identified and potentially prevented $240,000 in improper payments, with only modest inquiries or follow-up. By doing so, DEP could have ensured a more appropriate balance between distributing assistance quickly and protecting taxpayer funds from fraud, waste, and abuse.

B. Nine Recipients Failed to Disclose Other Sources of COVID-19 Assistance

OSC’s review revealed that at least 9 of the 24 Selected Recipients did not disclose other sources of COVID-19 assistance received, as required by the program guidelines. Specifically, all nine recipients had been approved for PPP loans in 2020, prior to submitting their applications to the program, but they did not disclose this information when filling out their applications. The amount of these undisclosed loans ranged from less than $1,000 to more than $200,000.

Of the recipients that did disclose other COVID-19 assistance, the information varied in accuracy and detail. Some identified the source of assistance but not the amount. Some did not identify the source or identified the source in only vague detail (e.g. “Treasury grant” or “NJ grant” or “9,000.00 dollars”).

Regardless, even when the information was provided by applicants, it was not used by DEP in the calculation of eligibility or to calculate whether a recipient was made “more than whole.” By not using this potentially critical information related to other COVID-19 assistance received, DEP missed an opportunity to detect and prevent fraud, waste, abuse, and improper payments in this program.

C. Ten Recipients Were Made “More than Whole,” Resulting in Almost $2.4 Million in Excess Funding for Recipients

OSC also analyzed whether any of the Selected Recipients had been made “more than whole” by their receipt of assistance from the Fishery Program. According to program guidelines, if a recipient was made “more than whole,” the recipient was required to return the excess money to ASMFC. To calculate whether a recipient was made “more than whole,” recipients were instructed to add any COVID-19 assistance, except for any PPP funds that were not forgiven, to their 2020 annual revenue. If that total revenue figure exceeded their five-year average annual revenue, the recipient would be considered “more than whole.”

|

Total 2020 Annual Revenue = |

2020 Revenue + DEP Assistance + Other COVID-19 Assistance |

OSC reviewed documentation the Selected Recipients provided to support their reported revenue figures. Recipients provided an array of documents that ranged from tax returns to general ledger statements to bank statements.[4] OSC used these documents to determine recipients’ 2020 annual revenue and calculate recipients’ five-year average revenue for 2015 to 2019.[5] OSC then added any other COVID-19 assistance to the demonstrated 2020 revenue to determine the total 2020 annual revenue.[6]

Example Calculation of Total 2020 Annual Revenue

|

$150,000 (Total 2020 Annual Revenue) = |

$100,000 (2020 Revenue) + $ 20,000 (DEP Assistance) + $ 30,000 (Forgiven PPP loan) |

The total 2020 annual revenue was then compared to the five-year average annual revenue. If the total 2020 annual revenue exceeded the five-year average, OSC determined that the recipient had been made “more than whole.”

Through this analysis, OSC found that 10 of the 24 Selected Recipients were made “more than whole” in 2020. A total of $2,373,550 in Fishery Program assistance was provided to those 10 recipients in excess of their documented losses. This represents just over 22 percent of the funding distributed through Round 1 of the Fishery Program. The excess Fishery Program benefit ranged from $19,000 to nearly $600,000 for a single recipient.[7] As noted in Finding A above, OSC determined that one recipient applied twice, in two different sectors, improperly using the exact same revenue and loss information in both sectors.[8] This resulted in two payments to this recipient that made the recipient “more than whole.” See Exhibit B for additional detail on OSC’s “more than whole” findings.

To OSC’s knowledge, none of the 10 recipients identified by OSC has returned the excess funds. OSC has shared the names of these entities with DEP for its further review and appropriate action.

D. Numerous Recipients Misstated or Failed to Provide Support for Revenue Figures

As discussed above, OSC, through DEP, requested that the Selected Recipients provide documentation to support their annual revenue for the years 2015 to 2020, as well as their March to June revenue for 2015 to 2020. A review of the documentation revealed that in many cases, the reported March to June revenue figures did not match the recipients’ supporting documentation. As a result, in eight cases, the recipients’ actual revenue loss calculation differed from the loss calculation identified in their applications.[9] The variances for those 8 recipients ranged from just over $3,000 to almost $71,000. See Exhibit B for additional detail. DEP directly relied on these revenue figures to determine how much funding each recipient would receive from the program. By over-reporting a revenue loss, recipients received more assistance.

In addition, although most Selected Recipients did provide documentation, some failed to provide documentation or provided incomplete documentation. Moreover, the supporting documentation provided by the Selected Recipients varied widely, and some documents were more credible than others. Some documents contained handwritten notes or revenue adjustments that were not clearly explained.

Failure by some Selected Recipients to provide complete documentation hampered OSC’s ability to perform a complete “more than whole” and loss calculation analysis for these recipients. See Exhibit B for more detail on the documentation issues.

DEP's Response

OSC provided DEP with a discussion draft of this report and asked for comment on the findings and recommendations set forth herein. DEP’s response has been considered and, to the extent appropriate, incorporated into this report. In its response, DEP emphasized that it had been tasked with developing the Fishery Program on an emergent basis to ensure essential financial relief reached fishing businesses that were severely impacted by the pandemic as quickly and efficiently as possible. DEP stated that it consulted with state and federal partners to develop the program guidelines, which explicitly allowed for revenue self-certifications and self-reporting as to whether recipients were made more than whole. DEP noted that it did not fail to appreciate red flags, but it simply was not required to review revenue information or conduct post-payment reviews. DEP stated that OSC’s recommendations, outlined below, go beyond what is required by the federal awarding agency.

Yet, by accepting self-certifications of revenue loss even when red flags were present, relying on recipients to self-report whether they’d been made more than whole, and failing to consider other COVID-19 assistance received in calculating revenue loss, the Fishery Program was exposed to an increased risk of fraud, waste, and abuse. Indeed, OSC found that just over 22 percent of assistance provided through the program may have been improper. DEP could have conducted minimal due diligence on applications to identify at least some of these issues without sacrificing expediency.

Section 12005 of the CARES Act, which established the fund for the Fishery Program, prioritized the “rapid delivery of funds during the COVID-19 pandemic.” Other applicable federal guidance also emphasized the importance of prioritizing expediency in awarding federal funds to meet crucial needs during the pandemic.[10] However, that guidance also urged agencies to balance “the need for expediency with steps to mitigate risk of fraud, waste, abuse, and improper payments,” writing that:

Agencies must continue to use standard best practices that include the internal controls necessary for prudently planning for, awarding, and managing contracts, grants, loans, and other forms of assistance. Where the new relief legislation requires agencies to undertake new or modify existing activities that affect payments, agencies are to balance the imperatives of expediency and good stewardship.

Through this review, OSC found that DEP appears to have focused on expedience without taking adequate steps to mitigate the risk of fraud, waste, abuse, and improper payments.

Recommendations

In view of the findings in this report, OSC makes the following recommendations to DEP:

- DEP should perform reasonable due diligence checks to flag applications for fraud, waste, abuse, or improper payments in future rounds of assistance or future assistance programs. If necessary, DEP should train employees performing application reviews to identify potential fraud or improper payment red flags. Staff should be directed to follow up with recipients regarding questionable information.

- In light of identified risk in this program, DEP should develop plans to perform post-payment reviews of applications to detect fraud, waste, abuse, and improper payments.

- DEP should provide clear instructions to all recipients regarding how to calculate whether they have been made “more than whole” and remind recipients of this requirement. DEP should direct recipients who have been made “more than whole” how and where to return excess funds.

- For those recipients who failed to provide the necessary revenue information to support their eligibility, DEP should follow up to obtain the information and confirm that payment was proper.

Referrals

OSC has identified to DEP the recipients who were found to have been made “more than whole.” OSC urges DEP to review these findings and consult with the Office of the Attorney General, the NOAA, and/or ASMFC to determine appropriate next steps regarding the recoupment and possible reallocation of funds for other eligible purposes.

[1] New Jersey was allocated $11,247,242 under what was termed “Round 1” of the Program. Pursuant to the Consolidated Appropriations Act, 2021, New Jersey was allocated an additional $9,439,080 for “Round 2” of the Program. This report relates to only Round 1 funding.

[2] See Office of Management and Budget, April 10, 2020. Implementation Guidance for Supplemental Funding Provided in Response to the Coronavirus Disease 2019 (COVID-19), OMB M-20-21. Washington DC: OMB. Available at https://www.whitehouse.gov/wp-content/uploads/2020/04/Implementation-Guidance-for-Supplemental-Funding-Provided-in-Response.pdf (accessed March 20, 2022).

[3] Applicants could apply to multiple sectors, but had to provide revenue information for each sector individually.

[4] For the purposes of this review, OSC accepted the documentation provided, inclusive of any hand-written adjustments or alterations.

[5] According to program guidelines, if a business was inactive and reported zero revenue for a year, those inactive years were still to be used to calculate revenue loss, so long as the entity existed. However, if a business was not yet in existence, those years were not included in the revenue calculation.

[6] As noted above, the information provided related to other COVID-19 assistance varied in detail, but for the purposes of OSC’s “more than whole” analysis, if program recipients reported any other COVID-19 assistance, OSC included the amount of the assistance in the 2020 revenue calculation unless it clearly overlapped with an identified PPP loan.

[7] In some cases, the amount of the overage exceeded the amount of assistance provided by the Fishery Program. For example, the calculation may have shown an overage of $100,000 when comparing 2020 revenue to the five-year average, but the applicant received only $20,000 in assistance from the Fishery Program. In this example, OSC would only have identified $20,000 as the excess benefit potentially subject to return to ASMFC.

[8] Fisheries were permitted to apply to multiple sectors but were required to “provide their fisheries-related revenue information for each sector individually . . . Applicants who operate in multiple sectors cannot combine all of their fisheries-related revenue and apply only under one of the sectors.” In this case, the recipient reported a loss in each of the commercial/aquaculture and dealer/processor sectors. The recipient received funding for 80 percent for the commercial/aquaculture sector loss and 100 percent for the dealer/processor sector loss. The recipient did not provide documentation to support a loss in both sectors.

[9] OSC did not include recipients in its count if the variance in the loss calculation was less than $500.

[10] See Office of Management and Budget, April 10, 2020. Implementation Guidance for Supplemental Funding Provided in Response to the Coronavirus Disease 2019 (COVID-19), OMB M-20-21. Washington DC: OMB. Available at https://www.whitehouse.gov/wp-content/uploads/2020/04/Implementation-Guidance-for-Supplemental-Funding-Provided-in-Response.pdf (accessed March 20, 2022).

Press Contact

Megan Malloy

megan.malloy@osc.nj.gov

609.575.5863

Waste or Abuse

Report Fraud

Waste or Abuse