Department of the Treasury

Department of the Treasury

(TRENTON) – – State Treasurer Elizabeth Maher Muoio testified before the Senate Budget & Appropriations Committee at the State House today, providing a detailed update on improving revenue projections for the remainder of Fiscal Year 2021 through Fiscal Year 2022, and outlining the critical investments Gov. Phil Murphy has proposed to help New Jersey emerge from the pandemic stronger, fairer, and more resilient.

The following is a copy of her full testimony, as prepared for delivery:

Good morning, Chairman Sarlo, Vice Chair Cunningham, Budget Officer Oroho, members of the committee.

Thank you for the opportunity to come before you today to discuss Governor Murphy’s proposed budget for Fiscal Year 2022 (FY22).

As always, I’d like to start off by introducing my colleagues here at the table with me - Deputy Treasurer Catherine Brennan, and Martin Poethke, the Director of our Office of Revenue and Economic Analysis (OREA). We also have two familiar faces serving in new capacities this year. Lynn Azarchi, who you may remember as the former Deputy Director of the Office of Management and Budget (OMB), was appointed late last year as the new Acting Director of OMB upon Dave Ridolfino’s retirement. And Tariq Shabazz, who previously worked for both OMB and NJ TRANSIT, has been appointed the new Deputy Director of OMB.

I’d like to personally thank each of them, as well as my front office, and the staff of OMB, OREA, and a number of our other divisions, many of whom have joined us here today or are listening in remotely, for their tireless dedication and professionalism in putting this budget together.

What I’d like to do today is provide some perspective on Treasury’s experience navigating the fiscal impacts of a health crisis that is now over a year old.

If the public wants to follow along, my testimony, along with the charts I’ll be referencing, is posted on Treasury’s homepage at: www.state.nj.us/treasury.

I plan to walk you through the revenue story of the past 12 months and then we will be happy to answer any questions afterwards.

When Governor Murphy took office in January 2018, New Jersey faced many fiscal challenges and we had made steady progress in addressing those challenges up to and including the introduction of the FY21 budget last February. Working together, we had continued meeting the required annual 10% ramp-up in our pension payment, an obligation which was, and is, famously onerous thanks to decisions by both parties over the past two decades to neglect or ignore the required actuarial payment. We had begun to build up our woefully underfunded surplus, which we had inherited at just over 1%. We instituted reforms yielding hundreds of millions of dollars in health benefit savings; took measures to control debt costs; significantly reduced our reliance on “one-shot” non-recurring revenues; and made unprecedented investments in education and New Jersey Transit.

On February 25th of last year, the Governor presented his FY21 budget to the Legislature. The budget message was bold and optimistic. Twelve days later, the Governor declared a Public Health Emergency and we found ourselves in an uncertain and bleak economic reality with a proposed budget that essentially wasn’t worth the paper it was printed on.

The Economy and New Jersey Tax Revenues – What Happened in FY 2021?

Thus began a year-long revenue forecasting roller coaster ride of deep drops and rapid reversals.

National economic forecasts changed with unprecedented speed and scope during the unchartered territory presented by the global pandemic, together with massive federal economic intervention unlike any seen in modern times. Likewise, the tax revenue outlook has never been more volatile.

In the original, pre-COVID forecast issued 14 months ago at the time of the Governor’s FY21 Budget Address, total revenues were estimated at $41.2 billion. Roughly three weeks later, the global health pandemic had gripped the United States, and New Jersey and other states began a series of social distancing measures and business restrictions designed to “flatten the curve” and slow the spread of COVID-19 in order to save lives and prevent the medical system from becoming overwhelmed.

Economic forecasts rapidly deteriorated. For context, economists will typically differ in forecasts by just tenths of a percentage point, debating a 2.5% growth rate vs. a 2.7% growth rate and changing their forecasts once every three to six months. But in just the few weeks between mid-March and early April of last year, the national GDP growth forecasts changed almost daily, plummeting drastically in a matter of weeks.

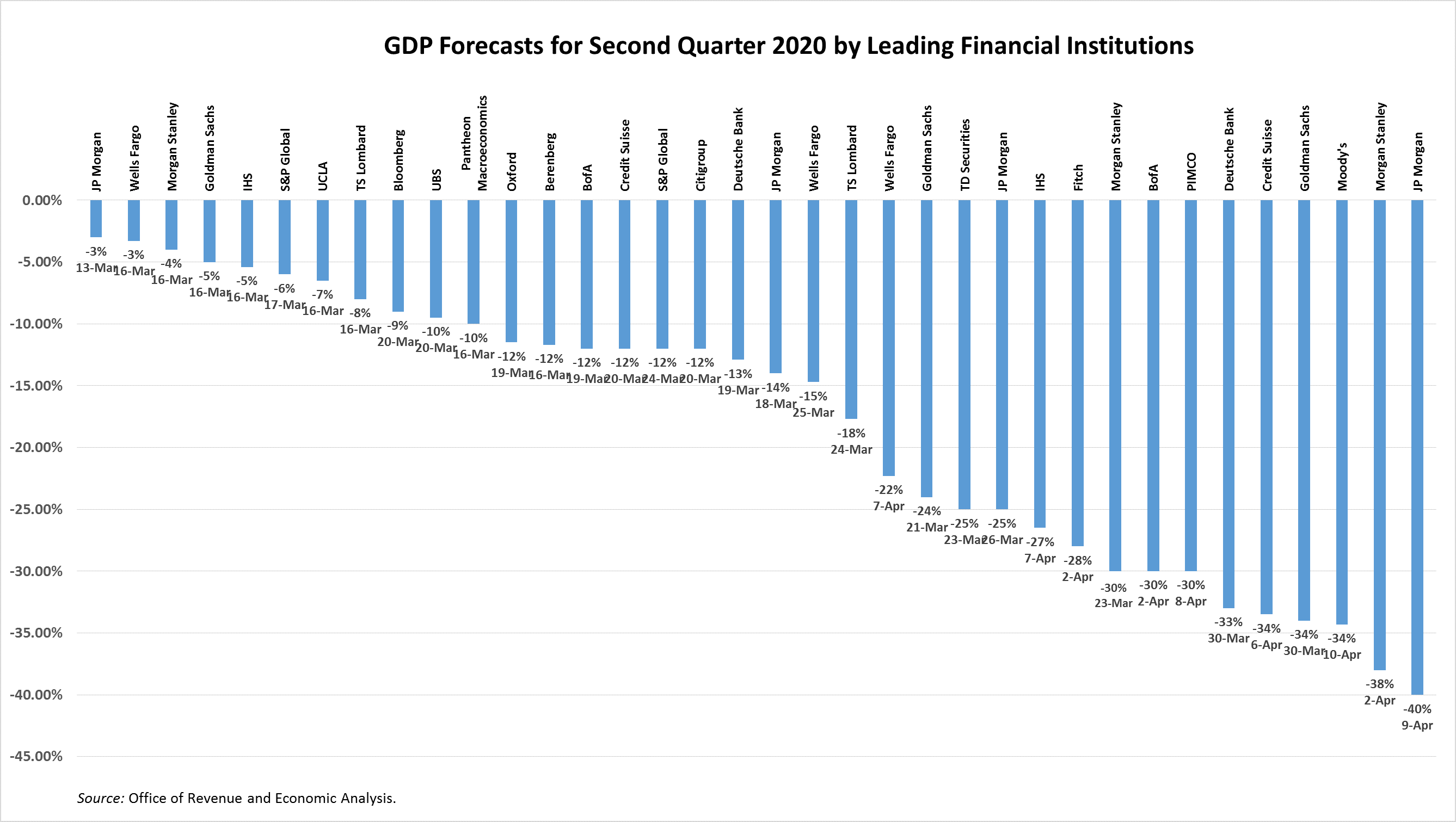

This first chart we included depicts the volatility in the rapidly changing forecasts for second quarter GDP from economists at leading financial institutions showing the extremely evolving forecasts in just under one month’s time. As the chart shows, in less than three weeks Morgan Stanley’s forecasts for the second quarter of 2020 dropped from -4% to -38%and in just under four weeks J.P. Morgan dropped from -3% to -40%.

U.S. second quarter GDP in 2020 fell by an unprecedented 32.8% on an annualized basis, while New Jersey’s GDP fell by an historic 36%.

As a result of the economic collapse, the IRS extended the tax filing deadline to mid-July and the Governor and the Legislature agreed to do the same, while also taking the unprecedented step of extending the fiscal year until September 30th to allow more time to get a handle on our revenue situation.

Treasury responded to the collapsing conditions with emergency budget forecasting and planning. Our revenue analysts and cash management staff have been working around the clock throughout the pandemic to analyze all of the data at their disposal and adjust our forecasts accordingly, based on the best information available at the time. As you know, there was no pandemic model to follow for this unprecedented crisis and we did not have the benefit of hindsight to inform our decisions in real time.

Treasury prepared two major budget reports following the onset of the pandemic and just prior to enactment of the FY21 budget. The first report issued on May 22, 2020 forecasted FY21 baseline revenues of $34.0 billion, which was $7.2 billion below the pre-COVID forecast. For clarity – baseline revenues are underlying revenues without the inclusion of any impact from policy or statutory changes or one-shots. The combined two-year revenue shortfall at this time was projected at $9.9 billion, including a $2.7 billion shortfall for the remaining months of FY20.

We were not alone in these estimations. Independent forecasters at Moody’s Analytics estimated a potential two-year baseline shortfall for New Jersey of $9.6 billion and a potential severe shortfall of $13.2 billion.

By the time we issued the second budget report on August 25th, with the benefit of delayed final tax collections, we saw an improvement in the revenue forecasts as COVID cases declined, business restrictions were eased, and the impact of the massive federal stimulus for individuals and businesses played out. The updated FY21 baseline revenue forecast in August was just over $35.5 billion - nearly $1.6 billion above the May 22nd forecast. The potential revenue shortfall eased, but still remained substantial at $5.6 billion.

With the adoption of the postponed FY21 Appropriations Act in late September, the State enacted an expansion of the tax on millionaires and an extension of the 2.5% CBT surtax rate. These policies yielded an estimated $600 million combined to help reduce the revenue shortfall. Total FY21 revenues were certified at $36.5 billion, which was a $946.6 million increase above the August report and included the $600 million from new tax policies and $346.6 million in higher baseline revenue forecasts.

At that time, the revenue shortfall compared to the original pre-COVID target was $4.7 billion. In addition, the revenue shortfall for FY20 settled in at $1.44 billion below the February 25 target. Combined, the two-year projected shortfall as of September was estimated at $6.1 billion, which was a notable improvement from the initial combined shortfall estimate of $9.9 billion.

The Governor and the Legislature worked collaboratively to establish a borrowing plan to help sustain New Jersey through the economic uncertainty in order to maintain the programs and services necessary to help residents and businesses most in need.

The State Supreme Court required a re-certification of revenues prior to the emergency borrowing bond issuance. At the beginning of November, just prior to going to market, a nationwide surge in COVID-19 cases, hospitalizations, and deaths was underway and a difficult winter was expected.

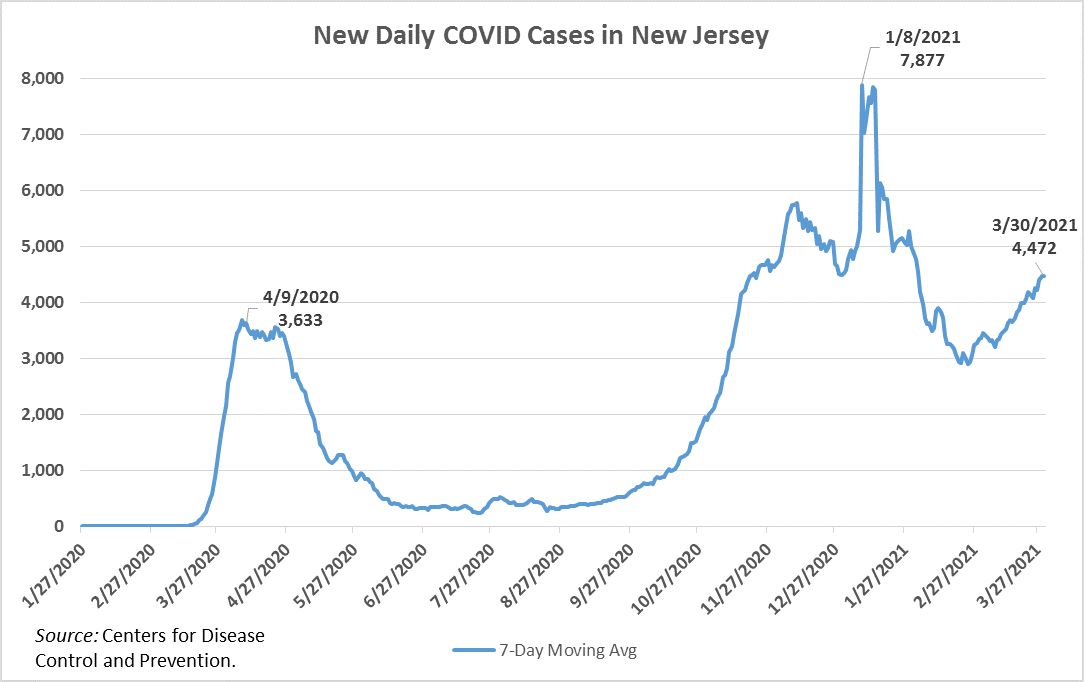

This next graph depicts the number of daily COVID-19 cases for New Jersey from the onset of the pandemic through last week, illustrating what we all now know – that the second wave far surpassed the first in terms of the number of daily reported cases.

Clearly we faced great economic uncertainty as we headed into the fall. When the FY21 revenue forecast was re-certified in early November, right before our bond issuance, total projected revenues stood at $36.9 billion, $397.9 million above the September certification. However, this still left us facing a $4.289 billion revenue shortfall, which served as the maximum emergency borrowing level.

As you know, the bond issuance was not something that was undertaken lightly. It was a joint decision made in tandem with the Legislature, at a time of enormous economic uncertainty during a once-in-a-century crisis.

We knew we were entering a second surge, the health effects of which are clearly illustrated in the chart above, and the Governor and Legislature did not have the luxury of hindsight to know the closures and economic fallout would not be as intense as they were in the spring despite the higher daily caseload of new COVID infections.

We couldn’t simply say, as some are now suggesting, let’s wait until later in the fiscal year to make the decision to borrow. First, remember we had already placed roughly a billion dollars of available appropriations into reserve, postponed more than half a billion in spending on critical obligations, and transferred our entire rainy day fund into the General Fund.

The Legislature approved an Appropriations Act that relied on resources that included the borrowing. The Governor then certified revenues that, together with the legislatively-approved borrowing, provided for a constitutionally-mandated balanced budget.

So, yes, while New Jersey, like the rest of the nation, suffered extraordinarily from the health tolls of the COVID-19 crisis, we did better than anyone expected economically.

Imagine, though, how disastrous it would have been if we had somehow postponed borrowing and the opposite panned out.

Imagine if, like the first wave, the economic ramifications of the second wave had mirrored the surge in cases.

Imagine if we faced an additional multi-billion dollar revenue hole, at the very time residents needed us most, and when we had already delayed a pension payment and school aid, and the fate of additional federal stimulus was entirely up in the air?

The lives and livelihoods of our residents were clearly not worth that very real risk.

So pursuant to the borrowing authority issued to us by the Legislature in the COVID-19 Emergency GO Borrowing Act, an issuance plan and an accompanying list of appropriations were presented to and duly authorized by the special legislative commission, as required by law. With the exception of minor changes reflecting actual appropriations, we have not deviated or added additional spending beyond that authorized list.

Significant Improvements in FY 2021 Revenue Forecasts Since November

As I’ve noted, our revenue analysts have adjusted our forecasts at every available opportunity based on the best information in real time. While the second surge had been well predicted, what could not have been predicted at that time was the fact that the economic impact would be much less severe and more manageable than during April and May. Economic forecasters have recently updated their projections pointing to a faster recovery to pre-COVID levels.

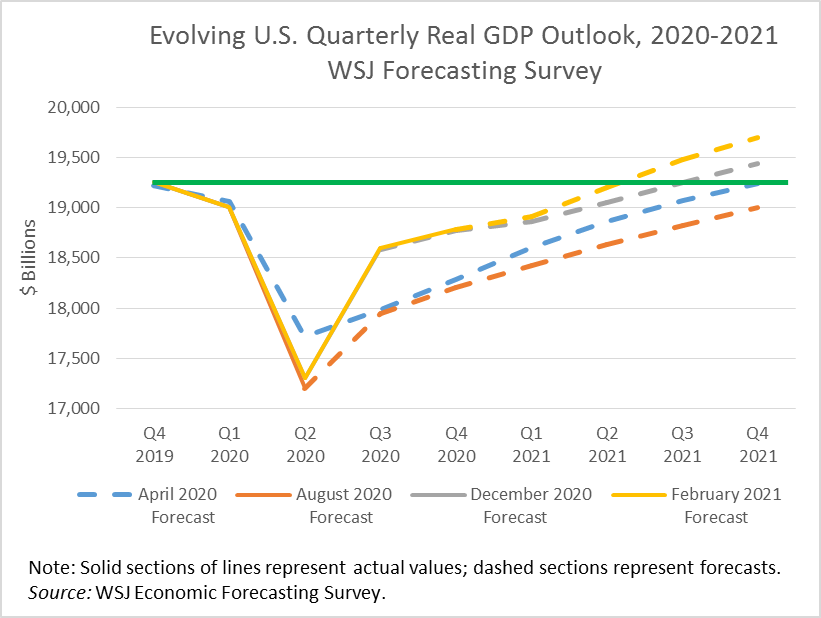

To get an idea of how national forecasts substantially changed as the pandemic progressed, this latest graph shows four sets of average U.S. GDP forecasts, as compiled by the monthly Wall Street Journal (WSJ) Forecasting Survey of economists. The April 2020 average forecast, which is the blue line, shows the early consensus for a historic drop in second quarter GDP, followed by steady growth and a return to pre-COVID levels by the fourth quarter of 2021.

Four months later, the August 2020 survey, which is the red line, showed a deteriorating outlook that was worse than in the April survey, with a deeper decline and a return to pre-COVID levels delayed further into 2022. This was the national consensus heading into our final budget planning.

However, after another four months, the December 2020 forecast survey, which is the grey line, showed a striking improvement from August. Pre-COVID GDP levels were viewed as possible by the third quarter of 2021.

Finally, the recent February forecast survey, which is the gold line, has the U.S. GDP returning to pre-COVID levels in the second quarter of 2021 - the least pessimistic perspective since before the pandemic.

So you can see that national experts have struggled to pinpoint the trajectory of the recovery and have adjusted their outlooks on numerous occasions.

The revised revenue forecasts in the Governor’s February Budget Message reflect the recently improved economic outlook and the resilience in State revenue collections. FY21 baseline revenue collections, excluding the emergency borrowing amount, are now forecasted at $39.9 billion, which is $3.4 billion above the September certification and $3.0 billion, or 8.2%, above the early-November re-certification. However, that still represents a $1.25 billion shortfall from our pre-COVID target.

New Jersey is not alone in this respect.

The National Conference of State Legislatures (NCSL) issued a state budget update a few weeks ago that noted, “While state general fund revenues are down from previous years in many states, revenue projections for the major tax categories have largely been adjusted upwards, and most states expect to meet or exceed revised estimates. This reflects a big turnaround from eight months ago when NCSL’s summer survey showed revenue losses looming large.”

Three Key Factors in the Improving Forecasts

The fact that the national economic outlook improved markedly during the winter is undeniable. The question is: why? Why do economic forecasters now think the economy will recover more quickly than during the Great Recession? What specific factors improved economic activity and, consequently, State revenue collections?

The following three factors are crucial, and somewhat interrelated. They also underscore what we all now know – which is that this pandemic has disproportionately impacted lower wage earners and increased the demand for safety net programs.

1) The unprecedented federal stimulus enacted in 2020 was more robust than during the Great Recession.

2) Economic closures eased sooner than most forecasted last summer and significant closures were avoided during the second wave of COVID cases in the fall and winter.

3) The K-shaped recession hit low-wage households while middle and high income households recovered more quickly.

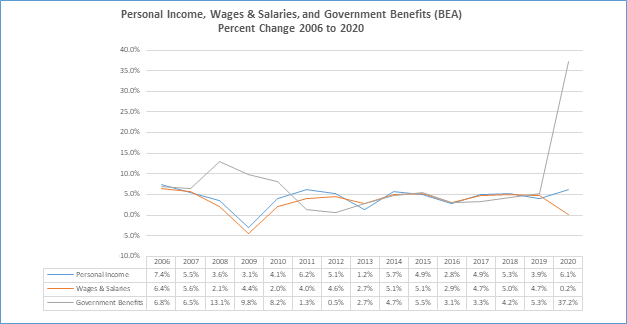

This next graph highlights a singularly crucial difference between the Pandemic Recession of 2020 and the Great Recession of 2008–2009: while federal support for household income grew in both recessions, it soared in 2020.

According to the Bureau of Economic Analysis, government benefits rose 13.1% in 2008 and 9.8% in 2009, but jumped by a remarkable 37.2% in 2020. While in 2009, national personal income declined 4.4%, tracking closely with wages and salaries, the opposite occurred in 2020. During the Pandemic Recession, national personal income is estimated to have actually grown by 6.1% — the best growth rate in a decade — even while wages and salaries were essentially flat, up only 0.2%, which is the worst rate in more than a decade.

Thanks to historic levels of federal income stimulus and support in 2020, households had plenty of cash to boost spending and stimulate the economy.

The Standout Story is the Sales Tax

That federal stimulus played a major role in boosting several of our revenue streams in ways that were not initially anticipated when the economy was in freefall.

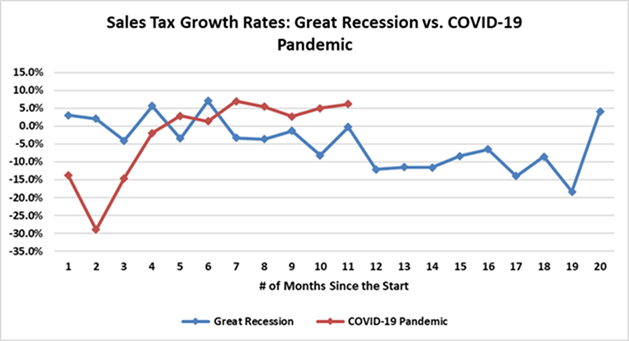

New Jersey’s Sales and Use Tax is the primary example of how normal behavior has been upended. While most tax revenues improved over last year’s May and August forecasts, the Sales Tax stands out as the biggest over-achiever and is worth looking at in some detail.

Treasury’s May 22 budget report anticipated a potential $1.5 billion shortfall from the original Sales Tax target of $10.8 billion for FY 2021. Fast forward to our latest forecast in the Governor’s February budget message and the Sales Tax is now estimated at $10.6 billion, only $151.2 million short of the original forecast, and nearly $1.4 billion higher than last May’s forecast.

The following graph shows Sales Tax revenue growth rates during the two recessions, tracked by the number of months into the recession.

Seven months into the Great Recession, which is the blue line, Sales Tax revenue collections turned consistently negative and declined for 12 consecutive months. By contrast, during the Pandemic Recession, which is the red line, Sales Tax revenue collections were down sharply for the first four months. However, they reversed course and have been growing positively since the fifth month, at times exceeding 5% growth above pre-pandemic levels. That is remarkable during a period in which GDP and employment levels have remained below the prior peak.

As I already noted, the massive federal stimulus has given households a substantial monetary boost, some of which has been spent and taxed. For example, tax collections from online and remote sales have soared during the pandemic, rising from about $408 million in FY20 to an estimated $546 million in FY21, which explains part of the Sales Tax’s resilience.

The unusual Sales Tax strength may also be due in part to a shift in consumer spending patterns away from many services that are not traditionally taxed to durable goods that are mostly taxable. Nationally, personal expenditures for durable goods was up 17.2%, year-over-year, in January while national expenditures for services were down 5.2%, year-over-year, in January and remain below pre-COVID levels, as people practice social distancing.

We’ve seen a similar boost in spending on home buying, which has been supported by historically low interest rates, federal stimulus payments, and a rise in work-from-home employment. As a result, we’ve witnessed a strong jump in Realty Transfer Fee revenues beginning last fall. Between September and January, Realty Transfer Fee collections have grown by between 19% and 49% above pre-pandemic levels each month. Additionally, the boom in home sales and home-improvements provides additional appetite for durable goods.

The Pass-Through Business Alternative Income Tax (PTBAIT)

In addition to the federal stimulus, which has provided households with a critical shot in the arm and helped improve certain tax revenue collections, the FY21 revenue forecast is also benefitting from a state tax policy change that will generate an unexpected one-time $606 million revenue boost. The Pass-Through Business Alternative Income Tax – or PTBAIT as we are calling it - was approved by the Legislature and signed into law last January to help provide relief to New Jersey taxpayers who have been hurt by the federal cap on the deduction for state and local taxes (SALT). The new law allows pass-through entities to elect to pay tax on proceeds that are distributed to its owners. In return, owners are able to claim a tax credit against their Corporation Business Tax (CBT) or Gross Income Tax (GIT) liability that is equal to their share of the pass-through entity’s tax liability.

This SALT cap solution didn’t get approval from the IRS until mid-November, after which we saw a startling $1.0 billion surge in payments to the State in late December, for taxpayers’ federal tax-planning purposes. Again, this is yet another area where we had no roadmap because no State-specific tax data previously existed to forecast elective PTBAIT behavior. We now expect about $1.3 billion in GIT and CBT tax credits to be claimed this spring, which will offset about $1.3 billion in PTBAIT payments, all related to Tax Year 2020. Over time this will be revenue neutral. However, an additional estimated $606 million of new spring estimated payments for Tax Year 2021 won’t be offset by credits until next year, creating a one-time revenue boost in FY21 that we could not have anticipated at the time of the budget enactment in late September.

So, our revised FY21 estimated revenue shortfall of $1.25 billion would be larger by $606 million if not for the one-time boost from PTBAIT.

What’s Next? The FY 2022 Appropriations Act and Additional Federal Stimulus

The revised FY21 revenue forecast, and the initial FY22 revenue forecast presented in the Governor’s February Budget Message, assume that the positive momentum in revenue collections seen since late fall will continue.

Total FY22 revenues are projected at $40.86 billion, which is $3.3 billion below the total level in FY21. When you exclude the $4.3 billion in FY21 emergency bonds, FY22 revenues are projected to grow by $952 million above FY21 for a 2.4% growth rate. Moreover, after additionally adjusting for the one-time PTBAIT net collection of $606 million in FY21, baseline recurring revenues are projected to grow by a more solid $1.558 billion, or 4.0%.

The State’s three largest tax revenues are all expected to increase year-over-year, which effectively accounts for most of the annual baseline revenue growth:

The GIT and the CBT are expected to recover from the pandemic-induced declines of FY21 and grow at rates above their long-run average trends. On the other hand, the Sales Tax has already seen a significant rebound in FY21 due to federal stimulus money boosting strong consumer spending, as I have already discussed. Consequently, while we expect the Sales Tax to continue to grow in FY22, that growth is expected to moderate as the federal stimulus fades and consumers return to more normal consumption patterns.

Among the other notable major tax streams, we are also projecting increases in Casino Revenues and Insurance Premium Taxes. This will be offset by declines in Realty Transfer Fee and Transfer Inheritance Tax collections, after an unusually strong year for those latter two sources in FY21. Petroleum Products and Motor Fuels Tax revenue are also expected to grow in FY22, as travel rises from lower levels during the pandemic. This will help replenish money dedicated to the Transportation Trust Fund.

For clarity’s sake, particularly in this rapidly changing environment, it is important to note that the forecast that OLS presented earlier today is informed by two extra months of data, whereas our forecasts are based on information available in early February when we prepared the Governor’s Budget Message. As always, we will issue a revised forecast later this spring. However, this year, we anticipate those updated numbers to now be available in June, rather than May, due to the recent extension of the tax filing deadline. Until then, Treasury will monitor collection numbers and follow the data and, as always, we will continue to work collaboratively with OLS revenue analysts on our forecasts.

Speaking of which, I’d like to take a moment to welcome Thomas Koenig as the new Legislative Budget and Finance Officer for OLS. Thomas is familiar to many of us through his work at OLS and highly respected, and we are pleased that the collaborative relationship established between our revenue analysts and OLS’ revenue analysts continues under his leadership.

Before I conclude, I would like to just briefly touch upon the issue of federal stimulus funding because I know we will go into this in greater detail in the afternoon hearing.

Right now we are eagerly awaiting federal guidance on how the funding from the recently enacted American Rescue Plan (ARP) can be spent. What we know for certain is that this will provide significant additional stimulus cash for individuals and businesses.

Direct federal stimulus in 2020 provided New Jersey households with a total of roughly $10.2 billion through two rounds of stimulus checks and $16.1 billion in supplemental unemployment assistance. Additionally, the ARP is delivering an estimated $9.6 billion in direct stimulus payments to New Jersey taxpayers. Federal supplemental unemployment benefits are now extended into September and could provide individuals with more than $8.0 billion, depending on actual unemployment levels and eligibility. Had the ARP not been enacted, we might have begun to see the impact on consumer spending fade sooner than we now expect in FY22. Instead, these direct infusions should help maintain the current positive trends.

The State is also slated to receive a total of $6.6 billion under the new ARP plan - $6.4 billion through the State Fiscal Recovery Fund and roughly $190 million through the Coronavirus Capital Projects Fund.

We are grateful for the federal assistance we’ve received to date and the additional aid we’ll be receiving soon.

People are still clearly struggling. Unemployment in late March was at 7.8%, roughly double what it was prior to the start of the pandemic, and we have still yet to recover roughly half the jobs that were lost last spring.

Continued federal assistance will be crucial in helping us weather this crisis, particularly in avoiding the mistakes of the past. We saw how long it took New Jersey to emerge from the Great Recession when state government chose to cut its way out of an economic crisis at a time when the demand for critical services skyrocketed.

As a result, we have chosen to invest our way out of the current crisis.

More than 90 economists and academics urged us to do so when preparing last year’s budget.

And economists across the country agree.

As do former fed chair Ben Bernanke and current chair Jerome Powell.

They’ve gone so far as to say it’s better to invest too much than too little during this precarious time.

So we are making critical investments in the people and programs who need it most, to get the state back on its feet and build a more resilient post-COVID future for New Jersey.

We are proposing a $200 million multi-departmental economic growth initiative that will boost economic recovery in New Jersey communities, provide access to capital for minority-owned businesses, and help government support sustainable economic growth.

We are delivering $319 million in direct tax rebates to over 760,000 middle-class families.

We are expanding the Earned Income Tax Credit, the Veteran’s Tax Deduction, and the Child and Dependent Care Tax Credit.

We are providing the highest level of school funding in history.

We’re making college more affordable and health care more accessible.

We are making the first full pension contribution in more than 25 years and a year earlier than anticipated.

We are reducing our debt issuance with significant direct appropriation investments that will also help stimulate the economy and we are examining ways to defease other existing debt.

In summary, we are investing in our economy, and more importantly, in our people, to help New Jerseyans get back on their feet, and provide the tools to make us all more resilient in the face of future challenges.

I look forward to taking your questions.

Official Site of The State of New Jersey

Official Site of The State of New Jersey